TechMagic Academy

TechMagic AcademyRetail Banking Digital Transformation: Shaping the Future of Financial Services

Last updated:21 March 2024

Retail banking is undergoing a significant shift, drastically accelerated by the COVID-19 pandemic. This event has significantly reshaped our expectations of banking. Customers have increasingly turned to digital tools for budgeting, planning, and investing, including using robo-advisors.

This article explores the transformative power of digitalization in retail banking, highlighting its crucial role in reshaping financial services. Read on for insights into the digital evolution.

Importance of Digital Transformation in Retail Banking

Digital innovation in retail banking is no longer an option but a necessity. Financial services executives are now tasked with leveraging digital transformation as a strategic tool to guide banks toward achieving their business goals, ensuring that services are instant, accessible, and tailored across various digital platforms.

This paradigm shift is driven by changing consumer behaviors, heightened competition from fintech companies, and the imperative need for operational efficiency. Embracing true digital transformation allows us to meet growing users' expectations for instant, accessible, and personalized services across multiple digital channels. Digital agility becomes paramount, enabling banks to navigate the complexities of the digital landscape efficiently.

Moreover, digital transformation paves the way for innovative financial models, from mobile banking apps to digital mobile wallets, making services more inclusive and accessible to a broader population. As such, digital transformation stands as the cornerstone for banks aiming to remain competitive, increase satisfaction, and unlock new growth opportunities in the digital age.

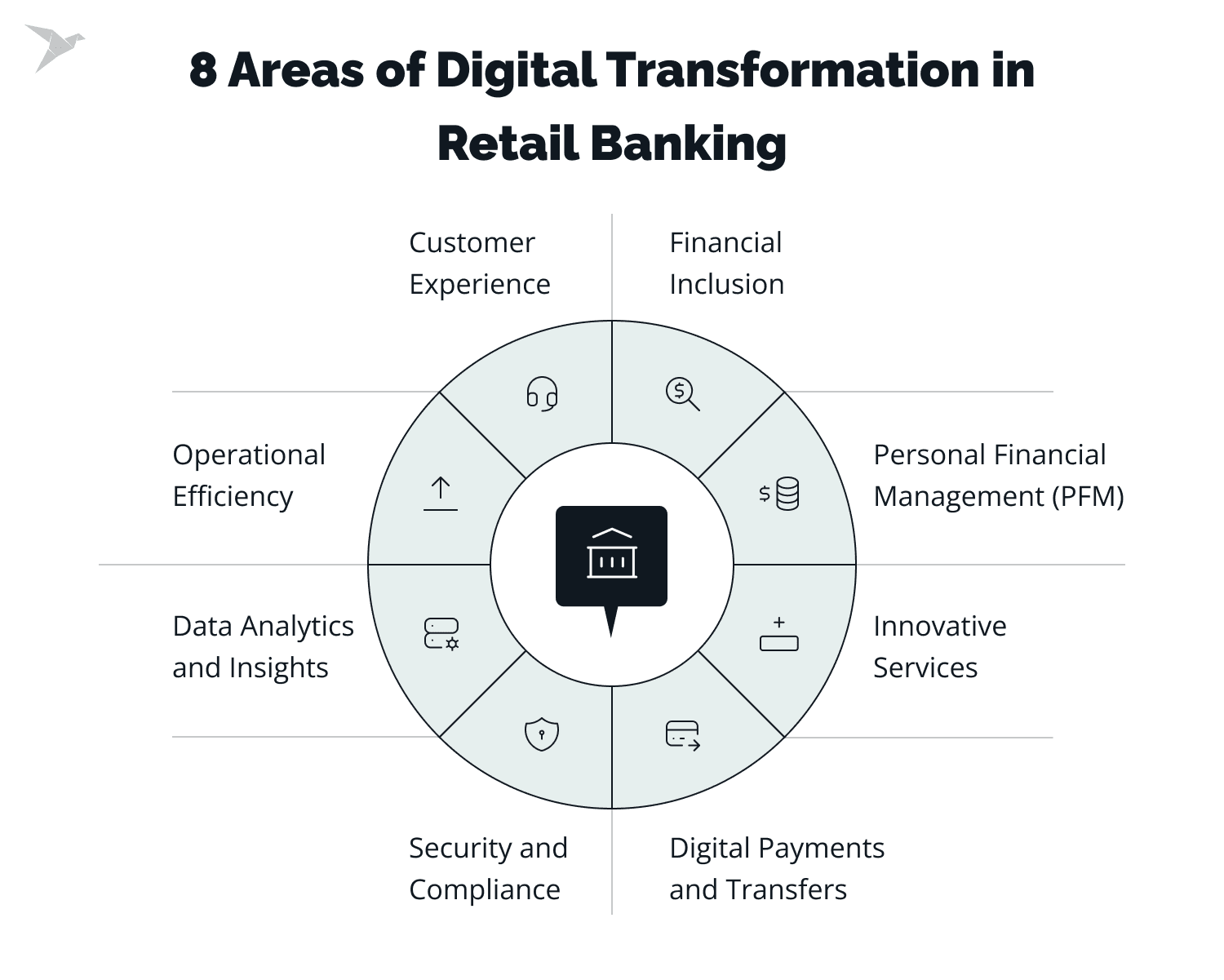

Here are the key areas of retail banking transformation:

- Customer Experience

- Operational Efficiency

- Data Analytics and Insights

- Security and Compliance

- Digital Payments and Transfers

- Financial Inclusion

- Personal Financial Management (PFM)

- Innovative Services

By focusing on these key areas, retail banks are not only adapting to the digital age but are also setting new standards for convenience, security, and customer-centricity in the financial services industry.

Future Trends in Retail Banking

The retail banking sector continues to evolve in response to technological advancements and changing consumer expectations. We are expecting significant annual growth in the retail banking market during 2024-2031. In 2026, the market grew at a steady rate, and with the rising adoption of strategies by market leaders.

Key trends shaping the future of retail banking include:

- Digital Transformation

- Omnichannel Banking

- Enhancing customer service with AI

- Focus on Open Banking, BaaS, and Embedded Finance

- Blockchain Technology

For a deeper dive into these trends and their implications for 2026, download our free white paper. Gain insightful information directly in your inbox and stay ahead in the evolving world of the retail banking industry.

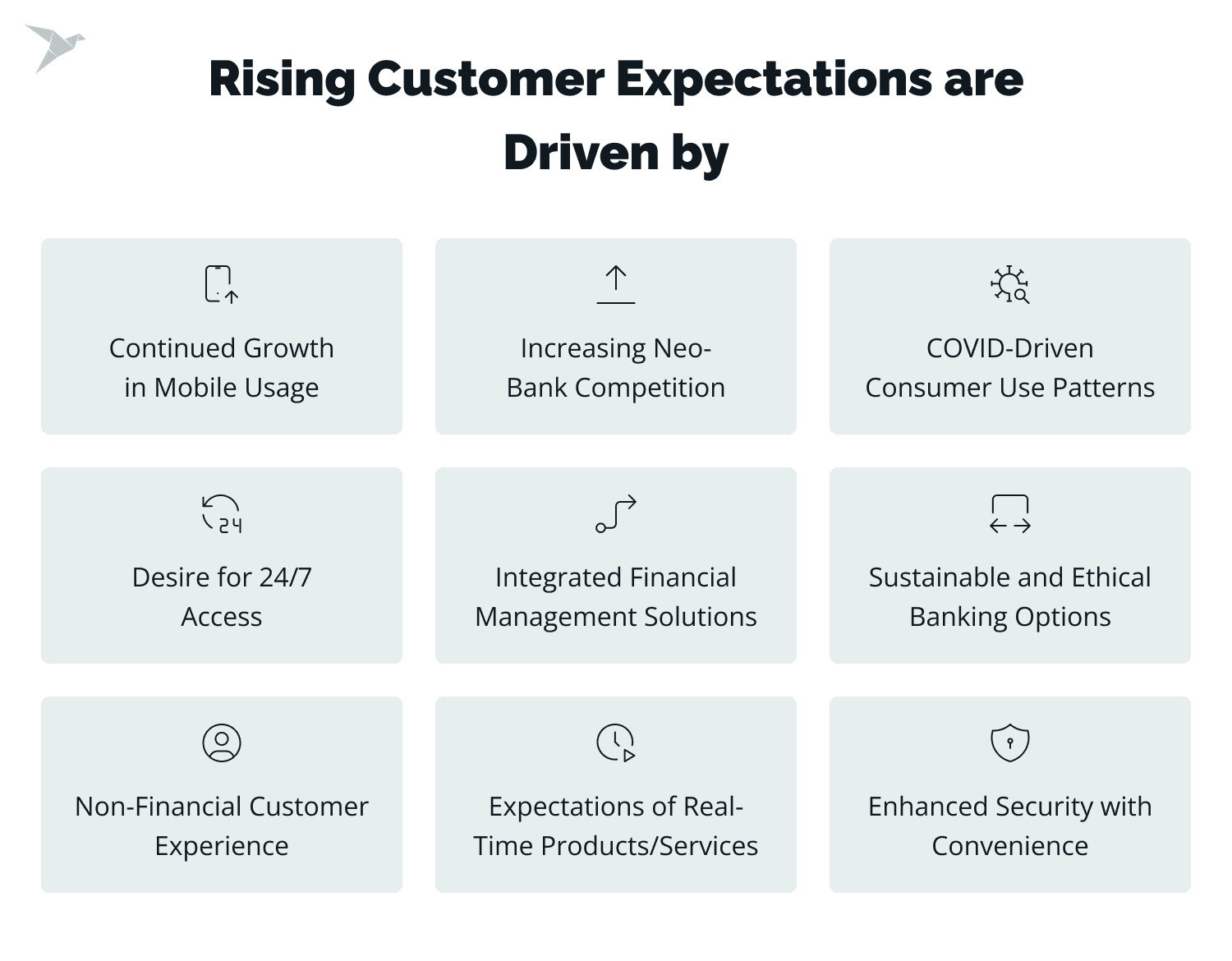

Overview of Changing Customer Expectations

In the evolving and competitive landscape of retail banking, several key factors are reshaping clients' expectations, compelling financial institutions to adapt and innovate to stay relevant. Here's a clearer look at them.

Continued Growth in Mobile Usage

The increase in smartphone adoption has made mobile the primary channel for the financial industry. This trend demands that banks optimize their mobile wallets, apps, and create user-friendly interfaces. Now ensuring features like mobile check deposits, easy transfers, and personalized alerts are standard offerings.

Increasing Neo-Bank Competition

Digital-first banks, or neo-banks, are setting high benchmarks for customer experience with their agile, innovative approaches to financial services. Traditional banks are thus compelled to rethink their digital strategies to compete with the seamless, efficient services offered by these challengers.

COVID-Driven Consumer Use Patterns

The pandemic has accelerated digital adoption among consumers, including demographics previously less inclined to use digital banking services. This shift has led to increased expectations for digital service delivery that is not only functional but also intuitive and engaging.

Non-Financial Customer Experience

Users increasingly judge their digital experience based on standards set by leading service providers from non-financial sectors, such as retail and technology. This comparison raises expectations for personalized communication, loyalty rewards, and innovative user interfaces.

Expectations of Real-Time Products/Services

The demand for instant gratification extends to the financial sector. Customers now expect real-time processing for payments, loan approvals, and account updates, driven by the capabilities of modern technology platforms.

Desire for 24/7 Access

The modern consumer expects to access the services at any time of the day without constraints. This requires incumbent banks to offer reliable, around-the-clock online services and customer support to address issues and inquiries instantly.

Enhanced Security with Convenience

As digital banking grows, so do security concerns. Customers expect robust security measures that do not compromise convenience, such as biometric authentication and single sign-on features.

Integrated Financial Management Solutions

There is a growing desire for financial platforms that offer more than just transactional capabilities, including budgeting tools, personalized financial insights, and integration with other services for a holistic view of personal finances.

Sustainable and Ethical Banking Options

Especially among younger consumers, there is an increasing expectation for financial institutions to demonstrate social responsibility, offer sustainable products, and invest in ethical practices.

These factors highlight the necessity for retail banks to continuously evolve, leveraging technology and data to meet the changing customer needs and expectations.

Learn about our expertise in the industry and what we have to offer

Enhanced Customer Experience

Customer experience has become a central focus for retail banks. A new reality for financial institutions looks like — if a customer does not get a good service, they may never return to the retail bank. Traditional, time-consuming processes are being reevaluated in light of digital advancements, with a shift towards more efficient, customer-centric models.

It has propelled incumbent banks to prioritize enhancing the customer experience, focusing on personalization, omnichannel access, and efficiency to meet and exceed customer demands and expectations.

Top Customer Experience Priorities in Retail Banking:

Personalization

Banks are leveraging advanced data analytics and artificial intelligence to understand individual customer preferences and behaviors. This deep insight allows for the delivery of personalized digital experiences, such as customized financial advice, tailored product recommendations, and proactive service alerts, making customers feel uniquely valued.

Omnichannel Methods

Recognizing that clients interact with their bank in multiple ways, including offline and digital channels. Retail banks are striving for a cohesive experience across all touchpoints. Whether it’s through mobile apps, online platforms, websites, call centers, or physical branches, the goal is to provide a consistent and seamless service. This includes features like synchronized account information and the ability to start a process on one channel and complete it on another.

Efficiency

Speed and convenience are crucial. Many banks are optimizing their processes to ensure quick and easy transactions, minimal waiting times, and fast resolution of queries and issues. This involves streamlining both front-end customer interactions and back-end operations, employing digital technologies such as robotic process automation (RPA) to automate routine tasks.

Organizations that excel at delivering effective customer experience reports:

- Increased customer loyalty (92%).

- Increased revenues (84%).

- Cost Reduction (79%).

FinTech firms that invest in customer experience trends have higher rates of recommendation, greater wallet share, and are more likely to up-sell or cross-sell products and services to existing clients.

Learn how we built macro-investing app with its own token and reward system

Importance of Seamless and User-Friendly Interfaces

Digital innovation has become the cornerstone of enhanced customer experiences. As the primary touchpoint for customers engaging with their finances online, the user interface (UI) and user experience (UX) play crucial roles in defining customer satisfaction and loyalty.

Key Features of Effective Interfaces:

- Clean and clutter-free design.

- Logical navigation and easy-to-use menus.

- Quick access to frequently used services.

- Personalized dashboard with relevant account insights.

- Secure and fast authentication methods.

The focus on developing seamless and user-friendly interfaces is not just about keeping up with digital trends. It's about providing a service that meets the evolving expectations of modern consumers.

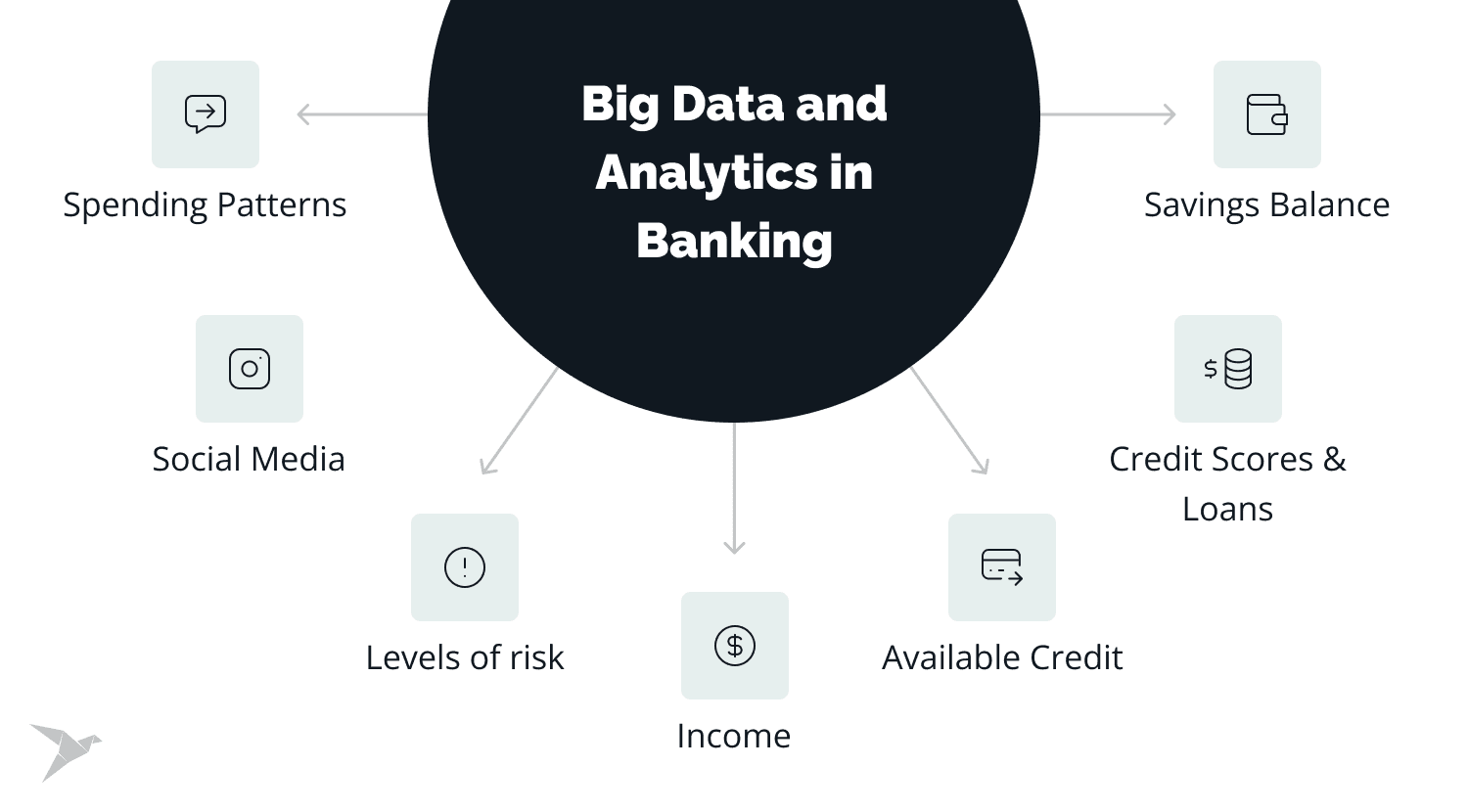

Big Data and Analytics for Personalization in Retail Banking

Enhancing the customer experience in retail banking demands an in-depth knowledge of your clientele, achieved by analyzing customer data from all angles.

The application of big data analytics is critical to improving the financial services experience, customer engagement, and guiding strategic decisions. As customer expectations continue to shift, leveraging big data is essential for gaining comprehensive insights into customer behavior and preferences.

Through analytics, banks can categorize clients, identify new opportunities, and develop predictive models to boost customer engagement and elevate the digital banking experience.

However, with the increasing utilization of customer data comes the critical importance of privacy considerations and the ethical use of data. Banks must navigate the delicate balance between personalization and privacy, ensuring that customer data is handled with the utmost integrity and in compliance with data protection laws. Implementing robust data governance practices and transparent data usage policies is essential to maintaining customer trust and loyalty. By prioritizing privacy and ethical considerations, banks can deliver personalized services that respect customer autonomy and safeguard their information.

Integration of Artificial Intelligence

Adoption of modern technologies like AI and machine learning can be game-changing for financial institutions. For example, a chatbot is the best solution for banks that can streamline simple, repetitive tasks such as checking account balances, credit card dues, or updating personal information, eliminating the need for human intervention. By programming chatbots to manage conversations effectively and adapt to customers' preferred communication styles and timings, banks can significantly reduce support requests and enhance team productivity. It all will lead to cost savings.

The adoption of chatbots in the banking industry offers several key advantages:

- Immediate Customer Support

In a digital era where customers expect swift assistance and 24/7 service, financial service chatbots provide instant responses to basic inquiries, ensuring customer engagement at any time. - Enhanced Self-Service Experience

Chatbots offer a conversational interface that mimics human interaction, catering to customers who favor self-service options for accessing information. - Personalized Financial Assistance

Integrated within fintech apps, chatbots can leverage user account data to furnish tailored information, assistance, and financial guidance, drawing on individual customer data for personalized service.

These applications of chatbots in the banking industry not only meet the modern customer's demand for quick and accessible support but also pave the way for more nuanced and individualized digital experiences.

Impact of Mobile Banking on Retail Banking

These services have transformed the way people manage their finances. This retail banking transformation has enabled customers to seamlessly conduct a wide range of financial transactions directly from their smartphones, fostering a culture of instant access and on-the-go banking. Nowadays, more and more consumers prefer using mobile apps to manage their finances. Customers can check their account balances and deposit checks using their smartphones, and they might even submit a mortgage application through their mobile device.

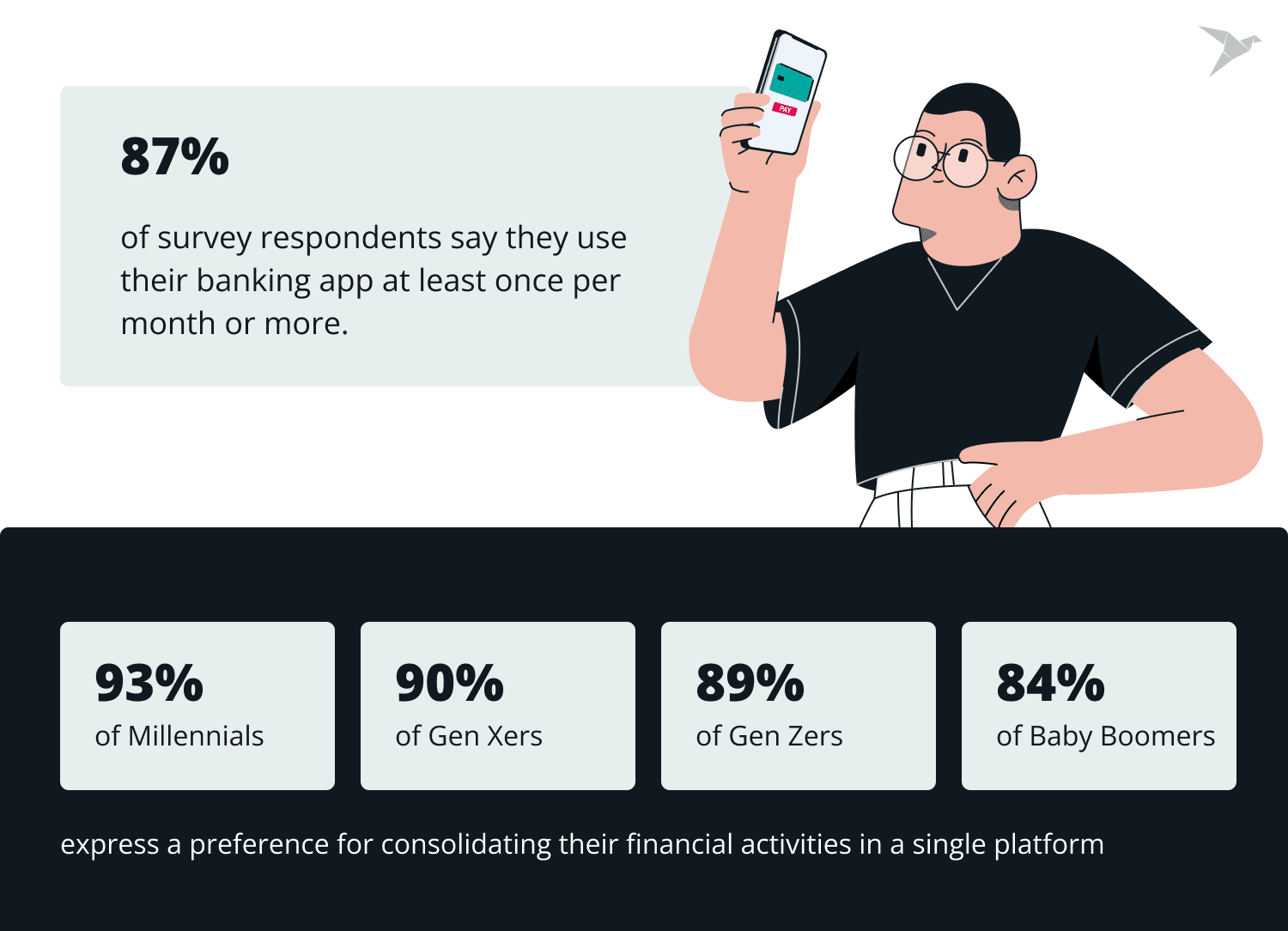

According to the Chase Digital Banking Attitudes Study consumers prefer mobile apps to computers. 87% of survey respondents say they use their banking app at least once per month or more.

The appeal of mobile financial services spans across various age groups, each demonstrating a strong preference for managing their financial needs in one digital space. At the same survey, we found out that

- 93% of Millennials

- 90% of Gen Xers

- 89% of Gen Zers

- 84% of Baby Boomers

express a preference for consolidating their activities within a single platform, highlighting the universal demand for integrated solutions.

In 2026, we are going to see an increase in mobile app users. According to the latest Chase Digital Banking Attitudes Study, which was conducted in December 2023, mobile app users grew by 10%.

Mobile Banking Features that Enhancing Customer Experiences

Mobile banking has introduced a wide array of features that have transformed the retail banking experience, making it more convenient, efficient, and personalized. Here are some of them.

- Account Opening and Management

It helps users easily open accounts, check their balances, view recent transactions, and monitor activity, all in real time from their mobile devices. - Mobile Check Deposit

Customers can deposit checks easily by snapping a photo with their smartphone, bypassing the need to visit a bank branch or ATM. - Bill Payments

It allows for easy setup and management of payments for utilities, credit cards, and more, including the option for automatic recurring payments. - Person-to-Person (P2P) Payments

Services such as Zelle, Venmo, or bank-specific platforms enable users to send money to others directly, usually without fees. - Mobile Wallet Integration

It often supports contactless payments through integration with services from big tech like Apple Pay, Google Pay, and Samsung Pay. - Credit Card and Loan Applications

Within the mobile app, customers can apply for loans and credit cards, monitor their application's progress, and receive timely updates. - Customizable Alerts and Notifications

The app offers tailored alerts for various activities, sending notifications through SMS, email, or directly within the app. - Financial Management Tools

Users benefit from built-in tools for budgeting, expense tracking, and financial goal setting, enhancing personal finance management. - Investment Services

It provides access to investment accounts and services, including stock trading and portfolio management, complete with customized advice. - Customer Support

Comprehensive in-app support is available, featuring live chat, ticket submissions, and a wealth of informational resources.

These features collectively offer a robust, secure, and convenient experience, catering to the diverse needs of today's digital-savvy consumers.

Branch Transformation

Today’s digitally savvy customers and the changing and competitive financial services landscape caused branch transformation. It means not just the physical layout of physical locations but also the integration of financial technology, enhancement of customer service, and the adoption of new operational and business models to deliver a more engaging and efficient customer experience. This shift helps branch employees to focus on more important tasks. Also, branch managers and other staff can leverage digital platforms to enhance in-person consultations, offering more customized financial advice and efficient service delivery.

The Objectives Behind Branch Transformation:

The driving forces behind branch transformation in retail banking include:

- Meeting the heightened expectations of digital-native customers.

- Combating the competitive pressure from online banks and fintech companies.

- Enhancing the profitability of physical branches in an increasingly digital world.

Branch transformation in retail banking is a strategic response to the digital revolution, aimed at creating a seamless blend of physical and digital banking experiences. By reimagining the role and design of branches, banks can not only improve client satisfaction and operational efficiency but also reinforce the relevance of their physical presence in the digital age. But the most important change is that now branches support digital, and are becoming advice centers.

Hybrid Models for In-Person and Digital Interactions in Retail Banking

The development of hybrid models that merge in-person services with digital capabilities is emerging as a strategic priority. These models are designed to offer customers the best of both worlds: the efficiency and accessibility of digital banking along with the personalized attention and expertise available at physical branches. This dual approach caters to the varied preferences of today’s customers, ensuring they have the flexibility to choose their preferred mode of interaction for different needs.

Benefits of Adopting Hybrid Models:

- Versatility

- Superior Customer Service

- Streamlined Operations

- Deeper Engagement

Conclusion

The retail banking transformation, accelerated by the COVID-19 pandemic, underscores the shift towards a more accessible, efficient, and personalized experience. This change, highlighted by the adoption of mobile financial services, artificial intelligence for improved customer interactions, and the integration of blockchain for secure transactions, underscores a broader movement towards a digital-first financial environment. Innovations like open banking and Banking as a Service (BaaS) further demonstrate the sector's move towards inclusivity and enhanced client experience, catering to customer demands for seamless, 24/7 financial solutions.

As we look towards the future, retail banking will undoubtedly continue to be shaped by the forces of digitalization and innovation. Banks that are agile, innovative, and customer-focused will not only navigate these changes successfully but will also lead the way in defining the future of financial services and finding new revenue streams.

FAQ

Digital transformation in retail banking is crucial for adapting to changing consumer behavior. It enables banks to offer a wider range of services accessible 24/7, improves security measures through advanced financial technology, and allows for the collection and analysis of data to provide personalized customer experiences. Furthermore, it drives innovation, helping banks to introduce new products and services more rapidly and to respond effectively to the competitive pressure from fintech companies. By embracing digital transformation, retail banks can increase their market share, enhance customer loyalty, and achieve significant cost savings by streamlining operations.

Personalization plays a pivotal role in enhancing the retail banking experience by tailoring services and communications to individual customer preferences and behaviors. This approach enables banks to deliver relevant financial advice, product recommendations and offers that resonate with each customer's unique needs and financial goals. As a result, customers enjoy a more engaging and satisfying financial journey. Personalization, driven by data analytics and AI, allows banks to create meaningful connections with their customers, setting the foundation for long-term relationships and improved client satisfaction.

It is a cornerstone of digital transformation in retail banking, serving as a critical interface that offers customers 24/7 access to financial services from anywhere. This accessibility and convenience not only meet the expectations of today's tech-savvy consumers but also drive the adoption of digital banking services, pushing traditional banks to innovate continually. By integrating advanced features such as biometric security, personalized financial insights, and instant customer support, it plays a pivotal role in modernizing the retail banking experience and fostering deeper customer engagement.