TechMagic Academy

TechMagic AcademyRevolutionising Banking: The Best Open Banking Apps

Last updated:4 March 2026

Years passed when traditional banking was the only option for managing your finances. With the rise of open banking, consumers can now access various innovative apps and services that offer a more personalised and streamlined banking experience.

Open banking banks revolutionize with a wide range of services, including rapid payments, budgeting, investments, and the verification of credit status and income.

Whether you're looking to simplify your budget, track your spending, or invest your savings, these open banking apps are created to help you make smarter financial decisions. With the added convenience of mobile banking and digital transactions, you can manage your money from anywhere, anytime.

In this post, we'll explore the top open banking market, advantages, solutions, best apps, and how open banking APIs work.

Key takeaways

- Open banking enables secure data sharing through APIs, giving users more control over their financial information.

- It helps businesses build better services using real-time financial data and integrations.

- Popular apps focus on account aggregation, budgeting, automated savings, and financial insights.

- Regulations like PSD2 play a key role in shaping how open banking works and ensuring data protection.

- AI, automation, and open finance will define the next phase of open banking development.

- The Payment Services Directive (PSD2) in the European Union requires banks to open up access to their customers' accounts to third-party providers with the customer's explicit consent.

What is Open Banking?

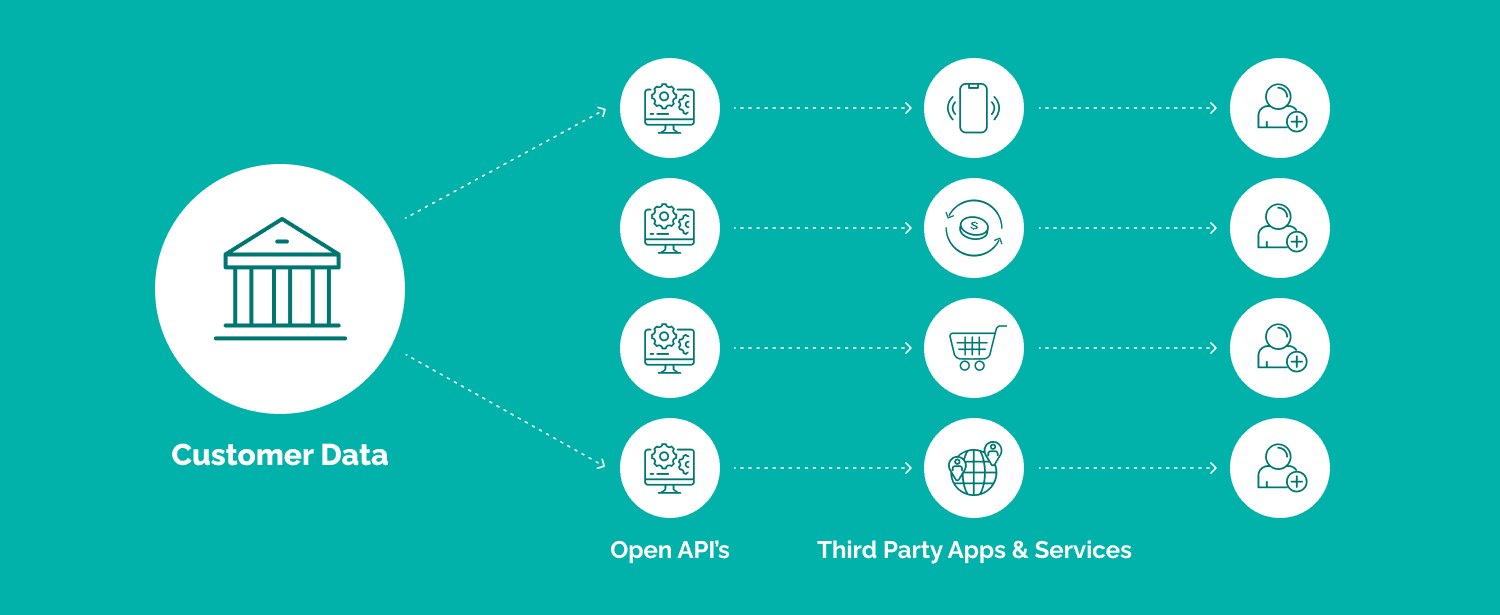

Open banking lets authorized third-party providers access banking data through APIs (Application Programming Interfaces), with the customer’s permission. Put simply, it allows financial information to move more securely between banks and other services instead of staying locked in one place.

That shift gives consumers more control over their data and opens the way for new financial services. For businesses, it means access to real-time financial information that can improve payment processing, account management, and product decisions.

It can also help non-financial companies add useful financial features, support faster fund transfers, strengthen risk management, and find new revenue opportunities.

With regulations such as PSD2 pushing adoption forward, open banking is becoming a practical way to deliver more secure, efficient, and personalized financial services.

Open banking, including API security, data protection, and customer authentication, is regulated by:

- The Payment Services Directive 2 (PSD2) in Europe.

- The Financial Conduct Authority (FCA) in the UK.

How does open banking work?

Traditional banking systems often keep data siloed within one institution. Open banking changes that by using standardized APIs and secure protocols that let approved providers connect to banks under a common framework. This makes data sharing more consistent and secure while also improving operational efficiency for banks, fintechs, and other connected services.

These APIs usually support three main functions: accessing account and transaction data, initiating payments or transfers, and sharing information about fin products. In other words, open banking helps banks and third parties work from the same playbook.

Customer Authorization

For a third-party provider to access a customer's data, the customer must first give explicit consent. This is usually done through the third-party provider's application, redirecting the customer to the bank's authorization page. The customer then logs in to their bank account and authorizes the third-party provider to access their data.

Data Sharing

Once the customer consents, the bank shares the customer's data with the third-party provider through an API. The API allows the third-party provider to retrieve the necessary data, such as transaction history and account balance, in a secure and standardized way.

Transaction Initiation

In addition to accessing customer data, open banking APIs allow third-party providers to initiate transactions. For example, a third-party provider could use an API to initiate payment directly from the customer's bank account without the need for the customer to log in to their online banking.

Security

Open banking APIs use various security measures to keep customer data safe. This includes encryption, two-factor authentication, and access controls to limit the data that third-party providers can access.

Overall, open banking APIs provide a way for third-party providers to access customer data and initiate transactions in a secure and standardized way. This allows for greater competition and innovation in the banking industry and gives customers greater control over their data and services.

Learn about our expertise in the industry and what we have to offer

Overview of The Current State of the Open Banking Industry

Many countries, including the UK and the EU, have already implemented open banking regulations. More are expected to follow in the coming years. As a result, a growing number of fintech startups and established financial institutions are building open banking solutions and services.

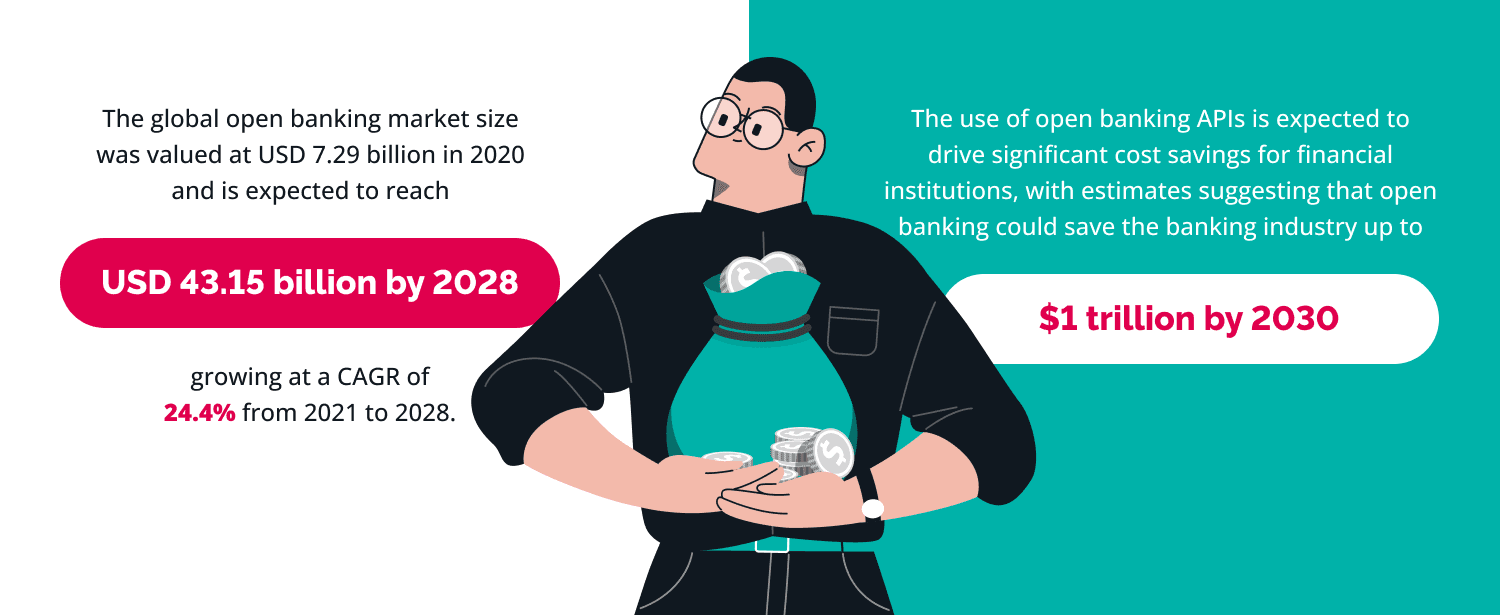

The global open banking market size is expected to reach USD 43.15 billion by 2028, growing at a CAGR of 24.4% from 2021 to 2028.

We summarise a few impressive facts about the open banking movement:

- The UK is a leading market for open banking, with over 300 fintech companies operating in the open banking space.

- Globally, open banking users are expected to exceed 645 million by 2029, reflecting steady growth as more services integrate financial data into everyday applications.

- The use of open banking APIs is expected to drive significant cost savings for financial institutions, with estimates suggesting that open banking could save the banking industry up to $1 trillion by 2030

Some key trends and innovations in the open banking industry include:

- Use of artificial intelligence (AI) and machine learning (ML) to analyze customer data and provide personalized financial services and products.

- Development of blockchain technology to enhance security, reduce fraud in open banking transactions, and implement digital wallet development service.

- Expansion of open banking beyond the financial sector to healthcare, energy, and telecom industries.

- Mobile app development services of open finance, which extends open banking principles to other financial products and services, such as insurance and pensions.

What are The Benefits of Open Banking Apps for Consumers and Businesses?

As a banking software development company, we cover benefits for both consumers and businesses.

Top Open Banking Apps

We've created a list of open banking apps that cover a wide range of needs, from personal budgeting and automated savings to business finance and infrastructure services. Some are built for end users who want a clearer view of their money, while others work behind the scenes to connect banks, apps, and financial data.

SoFi

SoFi is a fintech company that brings banking, investing, and lending into one place. It is designed for users who want a single view of their financial life. This makes it easier to manage several financial products without switching between separate apps.

**Key features: ** unified dashboard for accounts, investment tracking, loan management, spending insights

Rocket Money

Rocket Money focuses on helping users take control of subscriptions and everyday spending. It identifies recurring charges and helps manage them. The app is especially useful for people who want a clearer picture of where their money goes each month.

Key features: subscription tracking, bill monitoring, spending insights, cancellation assistance

Simplifi

Simplifi helps users plan their finances based on real behavior. It builds budgets from past spending and shows how money will flow over time. This gives users a more practical way to plan around everyday income and expenses.

Key features: personalized budgeting, cash flow projections, spending tracking, financial planning tools

Tink

Tink is a European open banking platform that enables apps to connect with bank data. It is widely used for account aggregation and payments. Its role is often behind the scenes, powering financial features inside other products and services.

Key features: account aggregation, payment initiation, data enrichment, API integration

Monarch

Monarch is a modern replacement for Mint that focuses on clarity and control. It provides a clean interface without ads. Many users choose it for a more focused and less distracting personal finance experience.

Key features: account aggregation, budgeting tools, goal tracking, ad-free experience

Revolut

Revolut combines digital banking with open banking features. Users can connect external accounts and manage everything in one place. This gives people a broader view of their finances beyond the Revolut wallet itself.

Key features: multi-account view, payments and transfers, budgeting tools, global financial services

YNAB (You Need a Budget)

YNAB is built around a structured budgeting method where every dollar has a purpose. It helps users plan ahead rather than track after spending. This approach appeals to people who want to be more intentional about how they use their money.

Key features: zero-based budgeting, goal setting, real-time updates, financial education tools

Exactly®

Exactly® provides open banking solutions for small and medium businesses. It focuses on simplifying financial operations and data access. It is particularly relevant for companies that need better visibility into cash flow and financial processes.

Key features: financial data integration, reporting tools, business insights, API connectivity

Coconut

Coconut is designed for freelancers and self-employed users who need simple financial management tools. It combines banking-related functions with support for tax and expense tracking. This makes it useful for people managing both personal income and business admin on their own.

Key features: expense tracking, tax estimation, invoicing, account aggregation

Bud

Bud allows users to connect multiple accounts and get a full picture of their finances in one place. It focuses on giving users and businesses more visibility through connected financial data. The platform is also used to support smarter fin products and services.

Key features: account aggregation, spending tracking, financial insights, API services

Digit

Digit helps users save money automatically by analyzing spending patterns and transferring small amounts into savings. The goal is to make saving feel more natural and less manual. It works well for users who want to build savings gradually in the background.

Key features: automated savings, spending analysis, goal tracking, balance monitoring

Plaid

Plaid is an infrastructure provider that connects apps to financial accounts. Many fintech products rely on it behind the scenes. In practice, it helps make secure data sharing between banks and apps much easier to implement.

Key features: secure account linking, data access APIs, transaction data, developer tools

Cleo

Cleo uses AI to help users understand their finances and make better decisions through conversational interaction. It presents budgeting and money insights in a more casual, chat-based format. This makes financial management feel less formal and often easier to engage with.

Key features: AI-powered insights, spending tracking, budgeting support, chat-based interface

Moneybox

Moneybox helps users save and invest small amounts regularly, often through round-ups from everyday purchases. It is built to make saving and investing feel more manageable over time. This approach works well for users who prefer steady habits over large one-time contributions.

Key features: round-up savings, investment accounts, goal tracking, automated deposits

Emma

Emma brings together multiple bank accounts and cards to help users track spending and avoid unnecessary costs. It is aimed at people who want more visibility and control across different providers. The app is especially helpful for spotting wasteful habits and repeated charges.

**Key features: ** account aggregation, spending categorization, subscription tracking, budgeting tools

Learn how we built macro-investing app with its own token and reward system

Plum

Plum automates savings by analyzing income and spending habits, then setting aside money in the background. It is designed to reduce the effort involved in building better financial habits. For many users, that makes saving feel more consistent and less dependent on willpower.

Key features: automated savings, budgeting tools, spending insights, investment options

Snoop

Snoop analyzes financial behavior and highlights opportunities to save money or reduce expenses. It focuses on practical suggestions based on real spending patterns. This makes it useful for users who want helpful prompts rather than detailed manual budgeting.

Key features: spending insights, savings suggestions, bill tracking, financial recommendations

Chip

Chip focuses on helping users grow their savings with better interest rates and automated deposits. It combines savings automation with products aimed at improving returns. The app is often positioned as a simple way to make cash savings work harder.

Key features: automated savings, interest accounts, goal tracking, direct payments

Zopa

Zopa uses open banking data to improve lending decisions and offer more personalized FinTech products. It combines this data-driven approach with consumer lending and savings services. That helps it tailor financial products more closely to each user’s situation.

Key features: lending solutions, credit assessment, savings accounts, financial insights

Lessons Learned From Failed Experiences

Not every fintech or open banking startup succeeds, but failed cases still offer useful lessons. They show how difficult it can be to enter a market shaped by strict regulation, strong competition, and high customer expectations. For many new players, the challenge is not only building a product, but also finding a place in a crowded financial ecosystem shaped by established financial organizations and growing user demands.

Regulatory compliance comes first

In financial services, compliance is not something a company can figure out later. Startups need to understand the rules early, secure the right licenses, and build products that meet legal and security requirements from the start.

This is especially important in open banking. Applications must follow regulatory requirements, consent rules, and obligations to protect data to receive approval from regulators.

Under frameworks such as PSD2 in the European Union, third party services can access account information only with the customer’s consent, and that consent can also be withdrawn at any time. This model depends on the secure exchange of consumer data, strong data security, and clear limits around how companies use a customer’s own data.

A good product still needs a clear market fit

Customer acquisition is often harder than expected. Even a well-designed product can struggle if it does not solve a clear problem or offer enough value to stand out.

For startups in this space, it is not enough to launch a useful feature. They need a clear proposition that matches a real customer need and gives people a reason to switch from existing financial tools.

That could mean better account information services, easier management of recurring payments, or tools that help people improve their financial health. The strongest products usually solve a practical problem while also supporting broader goals such as convenience, trust, and even financial inclusion.

Funding helps, but it does not solve everything

Strong funding can help a startup build faster, hire talent, and grow its product. But money alone does not guarantee success.

To survive in the long run, startups need more than investment. They need traction, a sustainable business model, and proof that the product can compete in the market.

That often means showing that the service can boost operational efficiency, maintain reliable service availability, and handle consumer data responsibly at scale. This is where many companies miss the boat: they raise capital, but fail to build a path to long-term growth in a market where third party services must prove real value.

Wrapping up

Open banking is already changing how people manage money, and this shift is still gaining speed across the financial services industry. Apps are becoming more connected, more automated, and easier to use, giving users better control over their finances without switching between multiple services. A strong open banking app can now combine budgeting, account aggregation, and payment initiation services in one place.

Looking ahead, several trends are likely to shape the next stage. AI-driven insights will become more accurate and proactive, open banking will expand into broader open finance services like insurance and investments, and integrations will move beyond banking into everyday platforms.

This also enables financial institutions, other financial institutions, and other financial service providers to work with more detailed financial data and build more innovative financial services. At the same time, security, consent management, and data transparency will remain a priority as the ecosystem grows.

For both businesses and users, the direction is clear: open banking is moving toward more connected, data-driven, and user-focused financial experiences. As the financial services sector evolves, open ecosystems and emerging payment technologies will continue to shape how financial products are built and delivered.

FAQ

Open banking applications are third-party applications that use the open banking infrastructure to offer consumers various financial services. They typically connect to a user's bank account and use their transaction data to offer budgeting, savings, investment, and loan management services.

Open banking apps must follow strict security standards to protect user data and support secure access to financial information. They typically use encryption and other safeguards to reduce the risk of exposing sensitive details during financial transactions. That said, users should still read the app’s terms, privacy policy, and consent settings before sharing their data, especially when using free banking apps.

Open banking apps use APIs to connect to a user’s bank account and retrieve the information needed to deliver a service. After the user gives permission, the app can access account data securely and use it for things like spending insights, payments, or account aggregation.

This model helps reshape the financial industry by enabling users to manage money across accounts more easily. Many budgeting apps rely on this approach, and it is becoming a standard way to serve open banking customers who want more flexibility and visibility.

Best open banking apps offer personalised financial advice, streamlined budgeting and savings tools, and access financial products and services from different providers. They can also help users make more informed financial decisions by providing insights into their spending and saving habits.