TechMagic Academy

TechMagic AcademyHow To Set Up A Digital Wallet: A Comprehensive Guide

Last updated:8 March 2026

When was the last time you made an online payment? Whether it was just moments ago when you ordered food or yesterday during shopping, online payments have become an integral part of our daily lives.

In fact, 4.4 billion people worldwide were using digital payments by 2025, accounting for more than half of the global population.

Among all online payment methods available, digital wallets stand out as electronic versions of your physical wallet, providing a secure and convenient way to pay for purchases without physical cards or cash. As the number of digital wallet users continues to rise, it's worth noting that 32% of them have multiple mobile wallet apps installed on their devices. Despite prominent players like Apple Pay, Google Pay, and PayPal dominating the market, there are still plenty of opportunities for innovative solutions.

Whether shopping in stores, online, or within apps, digital wallets provide seamless payment experiences, streamlining your money management and enhancing your overall payment processing strategy.

In this blog, we will delve into the critical aspects of creating a successful digital wallet app, including top features, digital wallet app development processes, challenges, security, compliance integration, technology stack, and more.

Key takeaways

- Digital wallets are becoming a mainstream payment method. Understanding how to set up digital wallet functionality helps businesses deliver faster, safer transactions for both online and in-store purchases.

- The demand for digital wallet development continues to grow as billions of users move toward mobile payments and contactless checkout experiences.

- Businesses planning how to create a digital wallet should focus on security, compliance, and integration with banks and payment networks to ensure reliable transactions.

- A successful wallet app combines core features such as payments, account management, expense tracking, and transaction history to improve everyday money management.

- Security is critical. Tokenization, encryption, and biometric authentication help protect sensitive payment data and reduce fraud risks.

What Is a Digital Wallet?

A digital wallet, also known as an electronic wallet, is a powerful financial transaction application that operates on various connected devices. Its primary function is to store your payment information in the cloud securely. Digital wallets come in various forms, including mobile wallets designed specifically for mobile devices and computer-accessible wallets.

Digital wallets are more than just financial applications; they are a hub for storing funds, enabling transactions, and tracking payment histories. In addition, they prioritize security by incorporating biometric authentication features like face ID and Touch ID, as well as multi-factor authentication and strong passwords, reducing fraud risks significantly.

But that's not all digital wallets can do. They offer a versatile storage solution for various items beyond payment methods. From gift cards, membership cards, and loyalty cards to coupons, event tickets, and even plane or transit tickets, the possibilities are vast. Moreover, digital wallets can verify a person's age when purchasing age-restricted items like alcohol.

How Does a Digital Wallet Work?

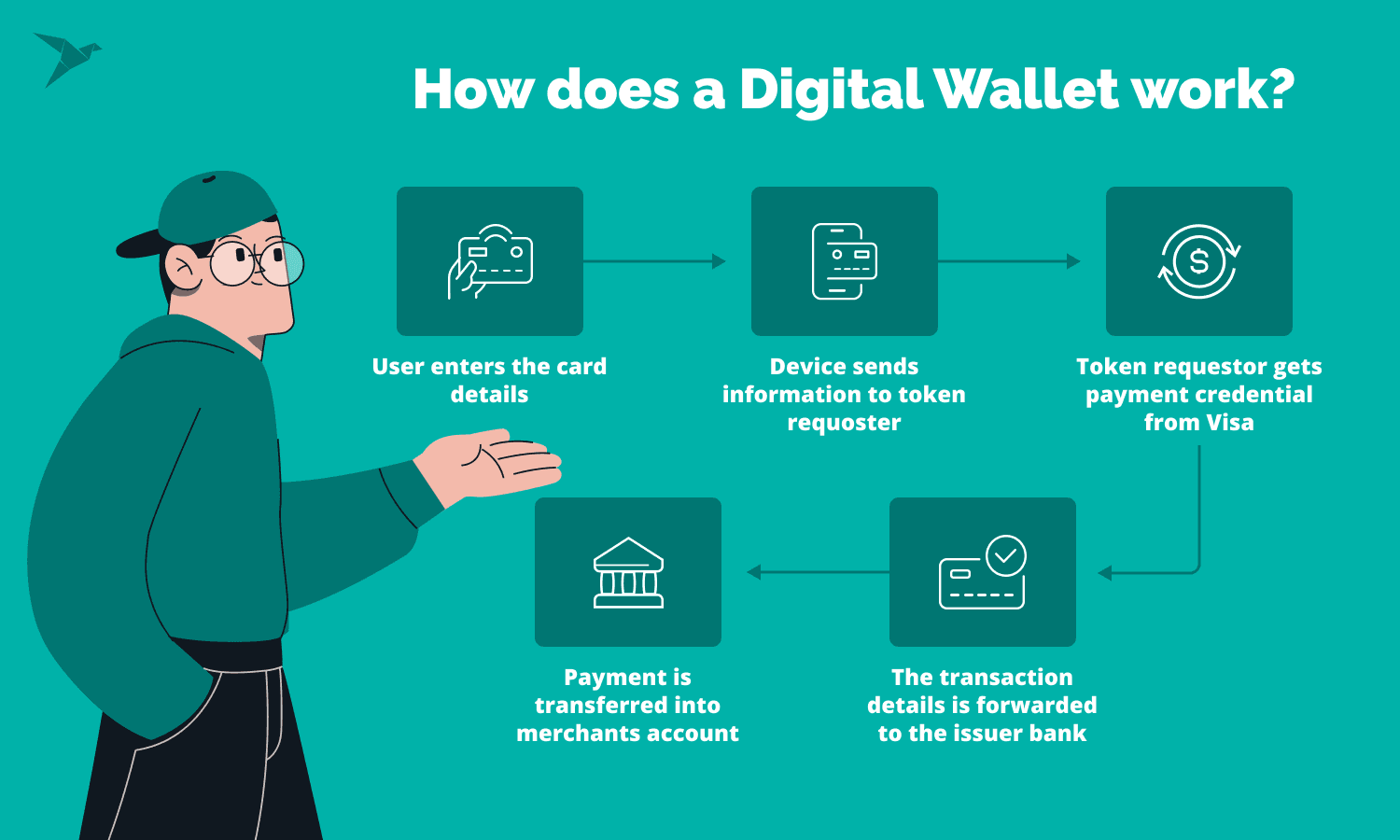

When a user initiates a transaction, the digital wallet transmits the chosen card information to the point-of-sale POS terminal. The terminal is connected to payment processors, through which the payment is routed via credit card networks and banks to complete the transaction.

Using a digital wallet involves a straightforward process for both online and in-person purchases. Users unlock the wallet app using facial recognition, fingerprint identification, or a PIN code and then choose their preferred payment method stored in the app. For online transactions, they proceed through the usual checkout process of the business, selecting the desired payment method within their mobile wallet.

In-person purchases rely on wireless and magnetic capabilities to transmit payment data from the user's device to a card reader or payment terminal. To complete the transaction, customers unlock their device, select the payment method, and hold it close to the card reader.

Learn about our expertise in the industry and what we have to offer

To complete transactions, different digital wallets employ distinct technologies:

- QR codes: These machine-readable barcodes can contain information about an item. Users can scan the QR code with their smartphone's camera to make payments. For instance, PayPal allows the generation of a QR code to facilitate in-store purchases.

- NFC (Near-Field Communication Technology): With an NFC-enabled device, such as a smartphone, you can simply tap it against a compatible point-of-sale terminal to complete the payment. This contactless method ensures a quick and secure transaction experience. Notable examples include Apple Pay and Google Pay, which rely on NFC for transactions.

- MST (Magnetic Secure Transmission): MST generates a magnetic signal resembling that of a traditional payment card when swiped. This enables quick on-the-go payments without the need to retrieve a physical wallet. Samsung Pay leverages MST technology. 93% of payment terminals in developed markets support NFC contactless payments.

- UPI (Unified Payment Interface): UPI is a real-time payment system that streamlines peer-to-peer inter-bank transactions through a single two-factor authentication process. It eliminates the need to enter sensitive data for each transaction repeatedly. Google Pay, Amazon Pay, and other apps use UPI technology.

Once the customer's payment information is transmitted using one of these technologies, the POS terminal or card reader routes the transaction data to the payment processor, communicating with the issuing and acquiring banks to process the purchase.

What Are the Digital Wallet Benefits?

Before delving into building a digital wallet, it's essential to explore the benefits of adopting this innovative payment solution. While some key benefits have already been outlined, let's delve deeper into additional advantages.

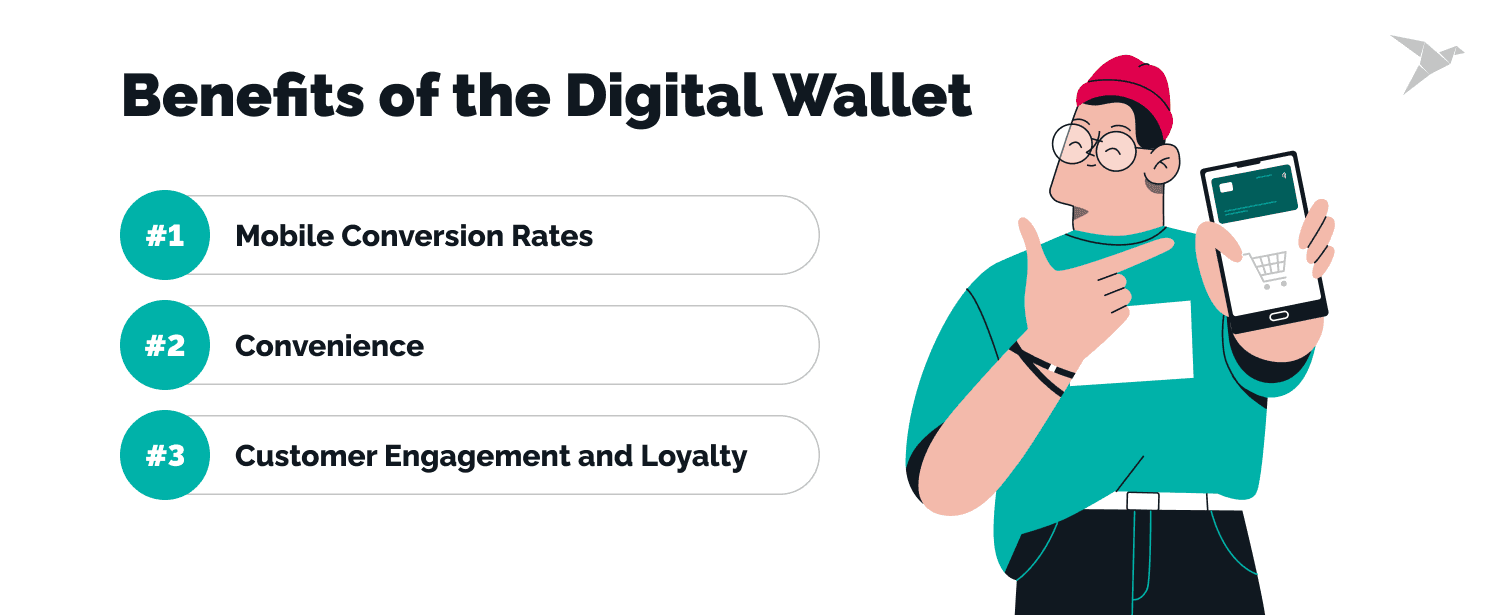

Customers prefer not to input credit card details on mobile devices during checkout manually. By accepting digital wallet payments for mobile purchases, businesses avoid abandoned carts and enjoy higher conversion rates.

Convenience

Wallet apps centralize all payment information, making transactions easier and faster. They eliminate the need to carry physical payment cards or cash, streamlining the payment process for users. For instance, PayPal offers a versatile platform for making online purchases, sending/receiving money, and contactless payments via QR codes.

Customer Engagement and Loyalty

The conventional credit card system often frustrates customers due to the many cards they need to manage, resulting in a lack of convenience. Provide customers with a centralized platform to streamline their payment methods, reducing the chaos of managing multiple credit cards. An example of successful customer loyalty is Starbucks' mobile wallet app, which allows users to pay for their coffee, earn rewards points, place advance orders, and skip queues.

Are Digital Wallets Safe?

Digital wallets provide a high level of security, primarily due to their use of tokenization and robust encryption during transactions. When a customer makes a purchase using a digital wallet, instead of transmitting their actual credit or debit card number, the wallet generates a unique one-time code, known as a token, which consists of random numbers.

This token is sent to the card reader for payment processing. In case of a data breach with the business or payment processor, any payments made through digital wallets remain secure because no actual card numbers were used and, therefore, cannot be stolen. Only the merchant's payment gateway can match this token to process the payment.

By combining encryption and tokenization, your information becomes unreadable and useless to fraudsters. Even if a retailer experiences a security breach, your personal payment data remains protected due to the multiple layers of security provided by digital wallets.

Moreover, most digital wallets go the extra mile to enhance security. They employ data encryption to protect your information from unauthorized access. Additionally, they require verification methods such as a PIN, password, or biometric authentication (e.g., fingerprint or facial recognition) to ensure that only authorized users can access the wallet. Compared to card transactions that rely on magstripes or EMV chips, digital wallets currently offer the most secure payment method available.

Talking about security, you may be interested in the free security checklist we composed for you.

Why Invest: Digital Wallets Market State

Curious why investing in a digital wallet app in 2023 is worthwhile? The following statistics will dispel any doubts:

Digital wallets are rapidly becoming the preferred payment method for online and in-person purchases. According to the Worldpay Global Payments Report, cash is expected to make up less than 10% of in-store spending in 2026, while digital wallets could reach 43%, becoming the most popular way to pay at the point of sale.

- The transformation towards electronic payments, particularly mobile payments, is steadily replacing traditional payment methods. Mordor Intelligence forecasts a staggering 29.5% growth in mobile payments between 2021 and 2026, while Juniper Research predicts a remarkable 60% increase in the value of digital wallet transactions by 2026.

- Between 2021 and 2026, mobile payments will experience a phenomenal CAGR of 24.5%, resulting in a $5399.6 billion market value, Mordor Intelligence.

- 32% of digital wallet users utilize three or more digital wallets.

- According to Statista, the mobile wallet market is poised for significant growth in the coming years. A new study by Juniper Research forecasts that the total number of digital wallet users worldwide will exceed 5.2 billion in 2026, compared to 3.4 billion in 2022, representing robust growth of over 53%.

Learn how we built macro-investing app with its own token and reward system

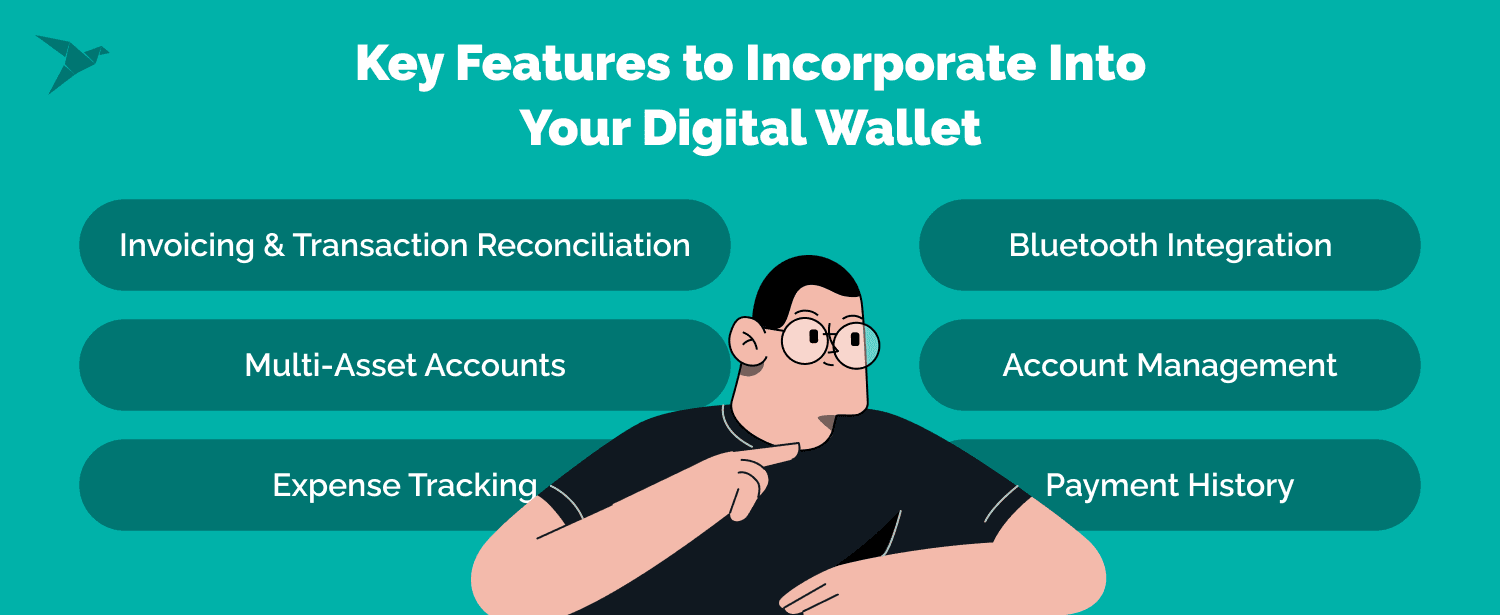

Key Features to Incorporate Into Your Digital Wallet

In crafting a strategy for digital wallet development, distinguishing between core and non-core features is crucial. Some essential functionalities to include in your finance-based application are as follows:

Invoicing and transaction reconciliation

To efficiently handle the reconciliation of transactions with various third-party systems like billing systems, IN, banks, and payment gateways, the digital wallet must incorporate an Auto Reconciliation Manager. This feature automates periodic reconciliations, including trust account reconciliation with partner banks, system e-value & biller's reconciliation, and bank to wallet and wallet to bank reconciliations, reducing manual efforts and streamlining the process.

Multi-asset accounts

Provide your customers with the convenience of holding funds in multiple currencies within their accounts. This feature caters to the needs of users with diverse international transactions.

Expense tracking

Enhance user experience by equipping your app with expense-tracking functionality. Allowing clients to monitor their spending fosters financial awareness and better money management.

Payment history

Transparency is key. Provide users with easy access to their transaction history, fostering customer loyalty and building trust between your app and its users.

Account management

Incorporate a feature for users to edit or update their bank account information, payment details, cards, and preferences, subject to a rigorous verification process for security.

Bluetooth integration

For physical store usability, consider integrating Bluetooth (and iBeacon for Apple devices) technology. When users are near Bluetooth beacons in a shop, the app can automatically open or send notifications about available deals, enhancing the in-store experience.

Other User Features include:

- Sign up via Social Login and seamless onboarding

- User Authentication

- Bank Account Integration

- Account Balance Check

- Contactless Money Transfer

- Bill Payments and Reminders

- Chat Support

- Push Notifications

- Loyalty & Rewards

- Bulk Payments

- Split Payments

Merchant Features include:

- Interactive Dashboard

- Product Management

- Profile Management

- Account Verification

- Customer Management

- Promotional Offers & Discounts

- Loyalty Points & Rewards

- Staff Management

- POS Integration

Admin Features include:

- QR Code Generation

- User & Merchant/Vendor Management

- Real-Time Analytics

- App Security Enhancement

- Reporting & Auditing

- Transaction Management

- App Support & Maintenance

- Dashboard Management

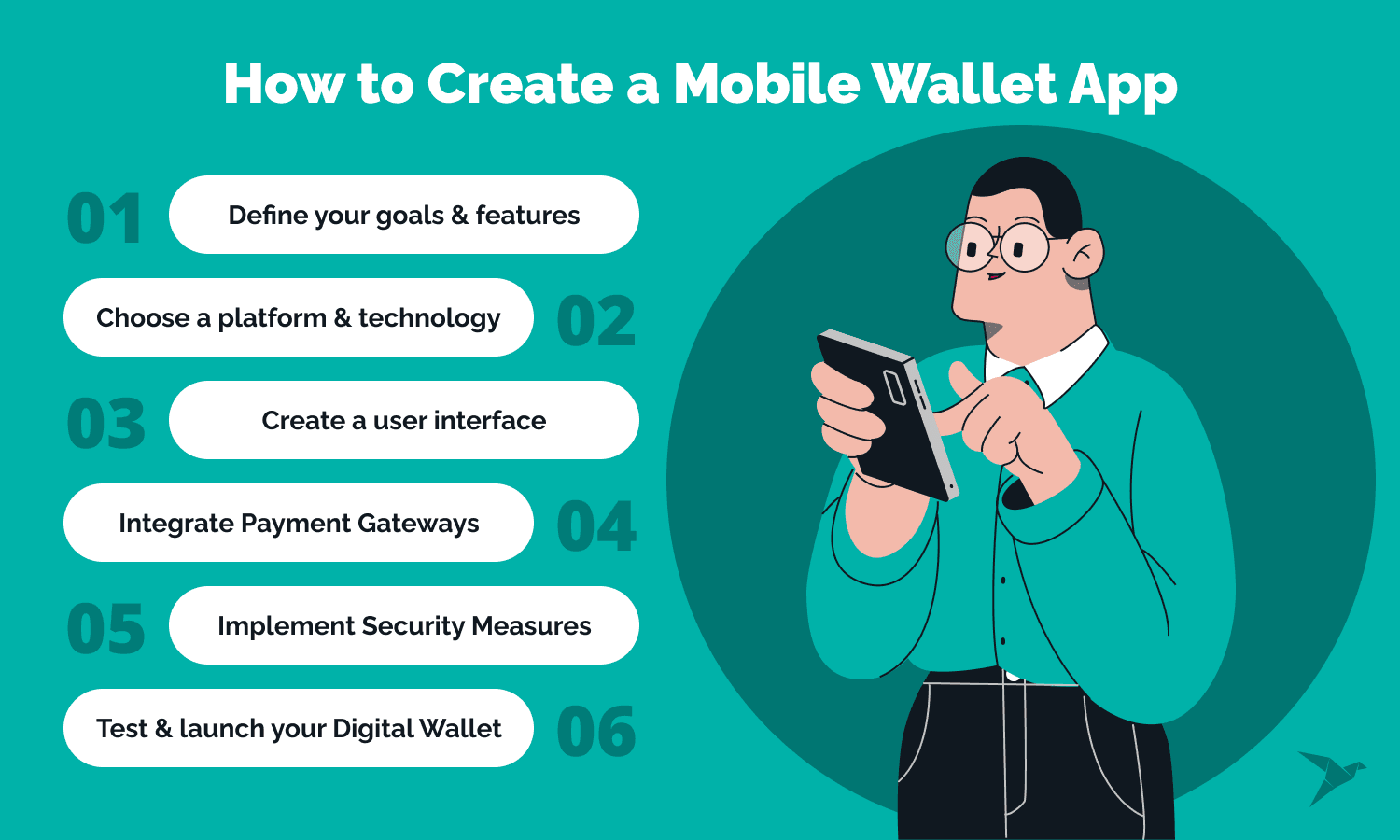

How to Create a Mobile Wallet App: Key 6 Steps

A successful digital wallet app development begins with product discovery, followed by UI/UX design, development, testing, deployment, product launch, and finally, maintenance and support. Let's delve into each phase.

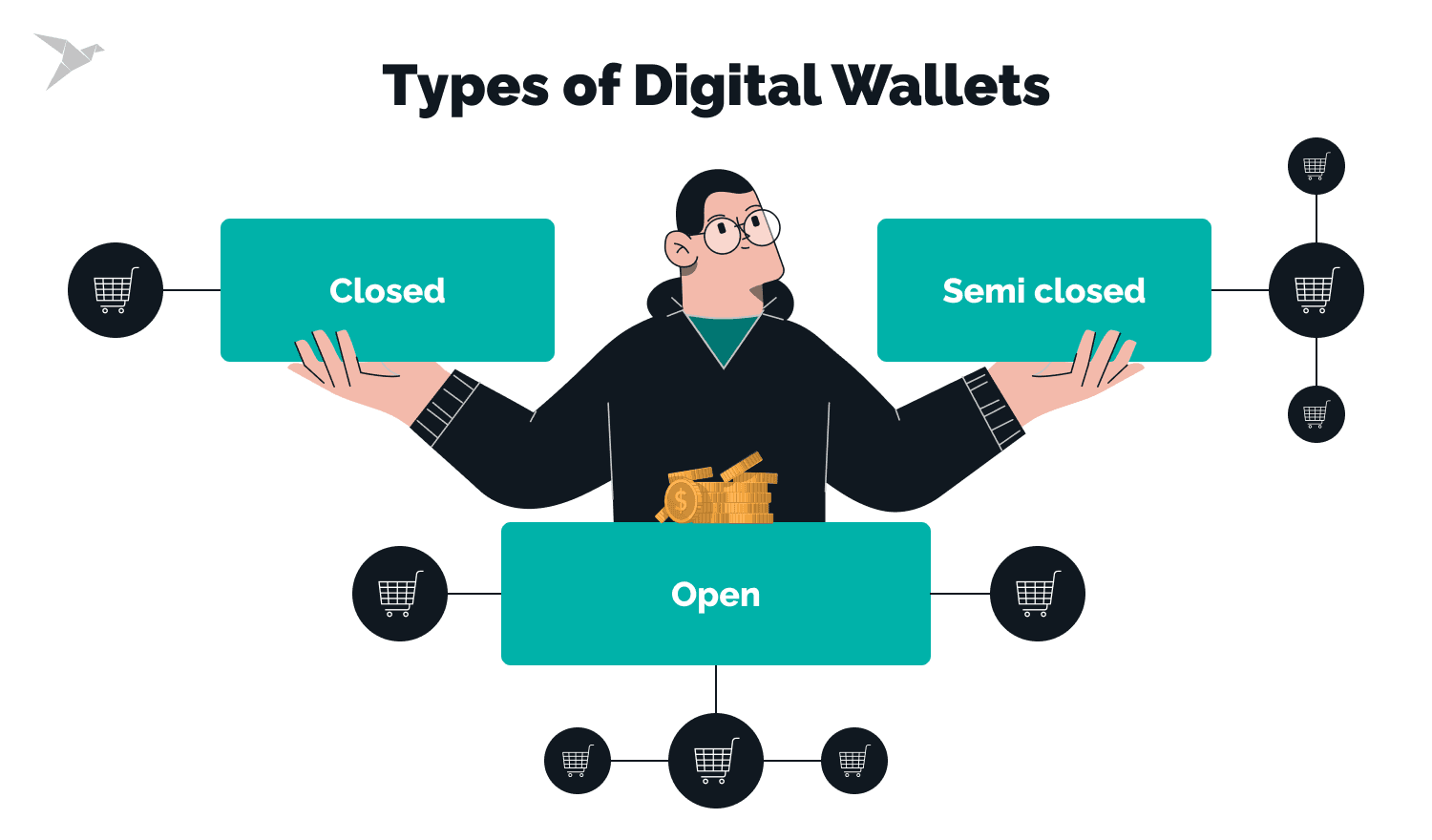

Step 1: Discover types of wallets

The initial step in mobile wallet app development is product discovery, where the project scope is identified and defined. Validate your business idea, test it with your target users, and determine the technical requirements for a successful mobile application.

Determine the type of mobile wallet you want to create - whether it's focused on payments, loyalty rewards, or other functionalities. Conduct thorough market research to understand the needs and preferences of your target audience. Analyze your competitors to identify their strengths and weaknesses, enabling you to develop unique features that set your app apart.

There are three main types of digital wallets, each with unique payment methods. From closed and semi-closed wallets with focused merchant relationships to open wallets backed by banks, and specialized wallets for cryptocurrencies, NFTs, IoT, and AI-powered solutions, users have many options based on their preferences and requirements.

Closed wallets

Closed wallets represent digital payment systems exclusive to a particular brand or merchant. Often referred to as "closed-loop," they restrict usage to specific merchants associated with the wallet. For instance, Starbucks' mobile app and Amazon Pay fall into this category.

One benefit of closed-loop wallets lies in their adaptability to the unique needs of a business. They also boast enhanced security as they aren't linked to customers' bank accounts or credit cards. Instead, customers fund these wallets in advance, reducing potential risks.

However, the usability limitation to a select number of merchants may inconvenience customers who prefer a single payment method for all their purchases.

Semi-closed wallets

Semi-closed wallets extend their services to multiple locations and merchants, striking a balance between closed and fully open wallets like credit or debit cards.

The advantage of semi-closed wallets is their increased flexibility, allowing transactions at a wider range of establishments. However, they may not offer the same level of security as closed-loop wallets, as they are integrated into a broader network of financial services.

Open wallets

Open digital wallets provide the highest level of flexibility, enabling purchases at any merchant accepting the associated payment method. They are not confined to a particular store or e-commerce platform and function wherever such payments are accepted.

Open wallets offer unparalleled convenience and might include additional features like expense tracking and reward point accumulation. However, it's essential to note that they may pose higher security risks compared to other types of digital wallets.

Step 2: Choose platform and tech stack

Select the platform for your digital wallet, which involves deciding between a native app or a cross-platform one. Native apps are designed for a specific mobile OS (e.g., iOS or Android), offering robust features and stability, but they require more resources and can be costlier. On the other hand, cross-platform apps share a single codebase across multiple platforms, such as Android, iOS, and web, resulting in cost savings but potential limitations on device-specific features.

Step 3: UI/UX design

Creating a prototype is a crucial step in visualizing your product. It involves building initial black-and-white screens, known as wireframes, to showcase the app's main flow. Prototyping allows you to identify design flaws early and address them to avoid escalating costs. Once the prototype is approved, your team can craft the user experience and user interface. For a digital wallet app, the design should prioritize intuitiveness and user-friendliness, adhering to a clear and consistent style.

The designing phase involves creating a user interface and user experience that provides an intuitive and visually appealing application for users to interact with and test. This phase also enables you to establish a brand logo, application icon, buttons, and other digital wallet features that distinguish your product from competitors.

Step 4: Develop an MVP and test

Rather than attempting to include all features from the start while thinking how to set up a digital wallet, we recommend to begin with an MVP. This involves implementing the core functionality of your app, such as adding payment methods and facilitating transactions. Once the MVP is ready, share it with your target audience and gather their feedback. This valuable input will guide further development and improvements.

The development team deploys cutting-edge technology stacks, sets up Continuous Integration and Continuous Deployment (CI/CD), and rigorously tests and validates the application's functionality. Thorough testing ensures the product behaves as intended and meets the highest quality standards.

You can employ a combination of automated and manual tests to evaluate the app's performance. As you may release your app on various platforms, comprehensive testing should cover a range of devices and operating systems.

Step 5: Launch

As mobile wallets are essentially mobile applications, they must be hosted on popular app stores like Google Play and Apple Store. By doing so, you make your application easily accessible for download by your target users, depending on their respective operating systems. A successful launch on these platforms boosts your app's visibility and allows you to reach a broader audience.

Step 6: Maintain

Regularly update your app to ensure compatibility with new OS features and improvements. This will not only enhance the app's performance but also provide users with a seamless experience across different devices and platforms.

In any app, minor bugs and issues may arise over time. Monitor user feedback and conduct thorough testing to identify and address these issues promptly.

Listen to your users' feedback and stay attuned to their evolving needs. Introduce new features and functionalities to meet their expectations and preferences. Adding valuable features will keep users engaged and encourage them to stay loyal to your app.

How To Set Up A Secure Digital Wallet

By using tokenized card details, retailers do not have access to your actual card number, minimizing the risk of fraudsters viewing or using your financial information.

Additionally, you can enhance security with

- Two-Factor Authentication (2FA): Requiring users to confirm transactions with an additional authentication factor, such as an SMS code or other identity verification, significantly enhances the app's security.

- Passcode and Biometric Authentication: Incorporate a unique password for logging into the application and regularly monitor your accounts for any suspicious activity, as it is a robust deterrent against intruders.

- Secure Data Transmission: To achieve secure and swift transaction experiences, implement SSL/TLS/VPN encryption, enabling safe data transfer between the application and the server.

- Point-to-Point Encryption (P2PE): From the moment you initiate a payment by swiping your phone over a Point-of-Sale (PoS) terminal, the encryption process starts and remains in place throughout the entire transaction.

Main Challenges Of Developing A Digital Wallet

Let's delve deeper into the key challenges you may face while considering how to create an e-wallet, and how to overcome them.

Compliance regulations

The financial industry is subject to strict regulations enforced by central banks. Digital payment apps must adhere to various compliance standards, such as Anti-Money Laundering (AML), Gramm-Leach-Bliley Act (GLBA), PCI (Payment Card Industry), and General Data Protection Regulation (GDPR) and Payment Services Directive 2 (PSD2) Strong Customer Authentication (SCA) in Europe. Navigating these regulations can be complex, especially as they vary from country to country and even within states.

Fraud detection & Risk mitigation

Fraud poses a significant challenge in digital wallet app development. Users unfamiliar with eWallets may be susceptible to scams and fraudulent activities. Common risks include data theft, data leaks, malware attacks, hacking, and more. However, developers can implement advanced technologies and security measures to mitigate these vulnerabilities.

Integration with existing systems

Digital wallet apps must often integrate with established payment systems like credit card networks and banks. Ensuring seamless integration with these systems may require collaboration with multiple partners and meticulous testing.

Conclusion

A modern digital wallet solution is a normal part of how people pay, shop, and manage money. Worldpay reports that digital wallets handled $13.9 trillion in global transaction value in 2023 and are projected to pass $25 trillion by 2027, reaching 49% of online and in-store sales combined. That shift creates real room for a digital wallet company with a clear product focus and a strong user experience.

Users expect simple payments on every mobile device

People want fast, low-friction payments on any mobile device. They want to pay in-store, check out online, and transfer money without extra steps. That is why the most popular digital wallets keep gaining traction. In many regions, users still prefer to fund wallets with credit and debit cards, which makes adoption easier for both customers and merchants.

The market is opening up for broader wallet products

This growth is shaping the wider banking and financial sector too. More digital wallet providers are expanding beyond basic checkout and moving closer to features users already know from mobile banking apps.

At the same time, interest in crypto wallets shows that people want more flexibility in how they store and use digital value. For product teams and financial institutions, that means wallet development is becoming less about one feature and more about building a complete payment experience.

The next few years look strong

The outlook is clear. By 2027, digital wallets are expected to account for almost 46% of global point-of-sale transactions, while cash is projected to fall to around 11%. That tells us one thing: the e wallet market will keep growing, and businesses that build useful, trusted products now will be in a stronger position later.

A good product still depends on the basics

Even with strong market demand, success still comes down to execution. Verification flows, security, compliance, and everyday usability all matter. A wallet can look promising on paper, but it only works if people can rely on it in real life.

If you have a project in mind or require assistance with digital wallet services, do not hesitate to reach out to us. We are here to support you and bring your vision to life.

FAQ

To create a digital wallet, you will need a reliable app development team that can design and build the application. Additionally, you'll require secure data storage infrastructure and integration with payment gateways or banking networks to create a mobile wallet.

Ensuring regulatory compliance and implementing robust security measures are also essential for the success of your digital wallet. Digital wallet apps must adhere to various compliance standards, such as Anti-Money Laundering (AML) and General Data Protection Regulation (GDPR).

Choosing the right digital wallet service provider is crucial for a seamless and secure experience. Consider factors like their track record, experience in the fintech industry, the range of services they offer, and their compliance with relevant regulations. Reading customer reviews and testimonials can also provide valuable insights into their reputation and customer satisfaction.

Yes, you can have multiple digital wallets. Many users choose to have multiple digital wallets for various purposes, such as personal and business use or to segregate different financial activities. Having multiple wallets can help you manage your finances more efficiently and cater to specific needs or preferences.