TechMagic Academy

TechMagic AcademyFinTech Fraud Prevention: Innovative Approaches to Securing Financial Transactions

Last updated:15 March 2024

The FinTech sector stands at the forefront of innovation. However, this progress is not without its challenges, and one of the most pressing concerns is the growing threat of fraud.

As the FinTech ecosystem expands, so does the sophistication and frequency of fraudulent schemes and activities, necessitating a vigilant and proactive approach towards fraud prevention.

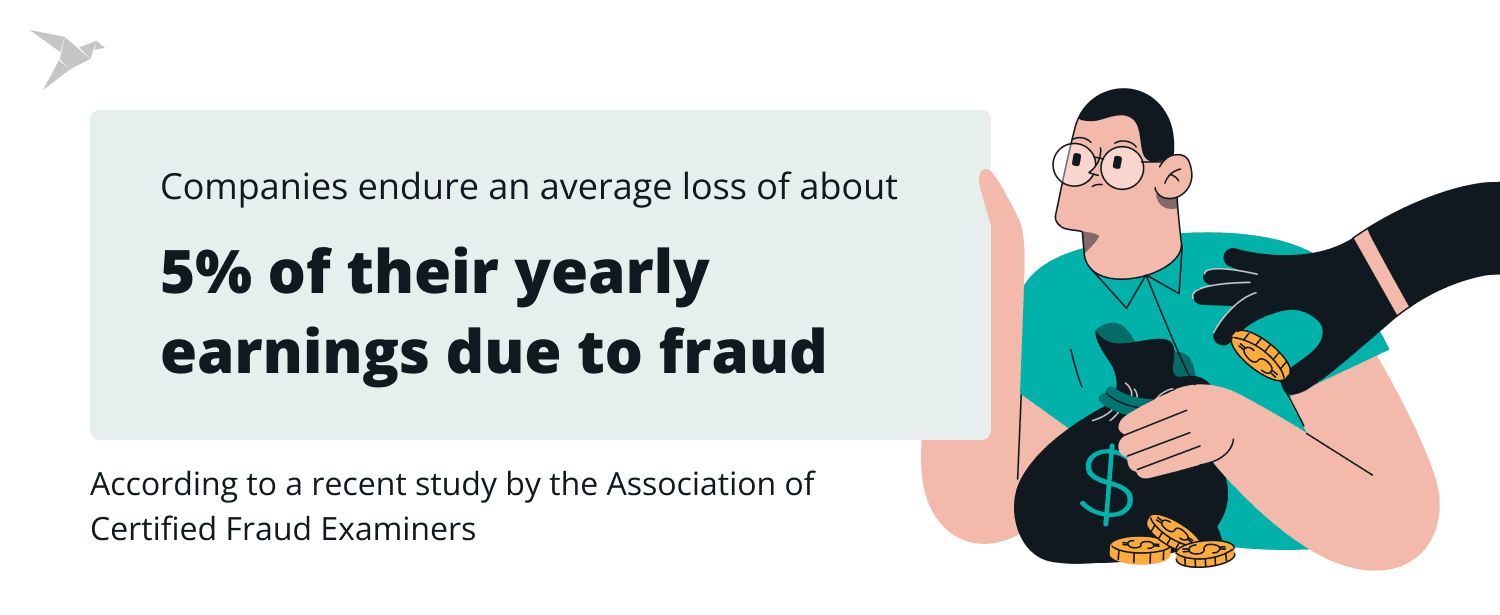

The magnitude of financial fraud extends far beyond the fintech sector, affecting organizations across industries. According to a recent study by the Association of Certified Fraud Examiners, companies endure an average loss of about 5% of their yearly earnings due to fraud. The impact is not confined to corporate entities; ordinary individuals reported an astonishing loss of nearly $8.8 billion to fraud in 2022 alone, marking a staggering 30% increase from the previous year. This alarming rise underscores the pervasive nature of fraud, influencing both large enterprises and everyday individuals.

PwC's recent research reveals a concerning statistic – 51% of businesses have encountered financial fraud within the last two years. Even more alarming is that these figures represent the highest recorded in 20 years.

As fraudsters intensify their efforts to exploit cybersecurity vulnerabilities within fintech firms, risk and compliance teams face heightened pressure to develop and implement robust strategies against fraud. Strengthening fraud prevention methods is important to strike a delicate balance between security and business growth.

We will explain the complexities of fraud in the FinTech sector and equip them with actionable strategies to fortify their defenses and ensure the resilience of their financial ecosystems.

What Are FinTech Fraud?

Understanding the landscape of fintech fraud necessitates an exploration of the prevalent types of fraudulent activities. Current statistics underscore the vulnerability of Fintechs, with an average fraud rate of 0.30%—twice as high as credit card fraud rates (0.15 to 0.20%) and triple the debit card fraud rate (0.10%).

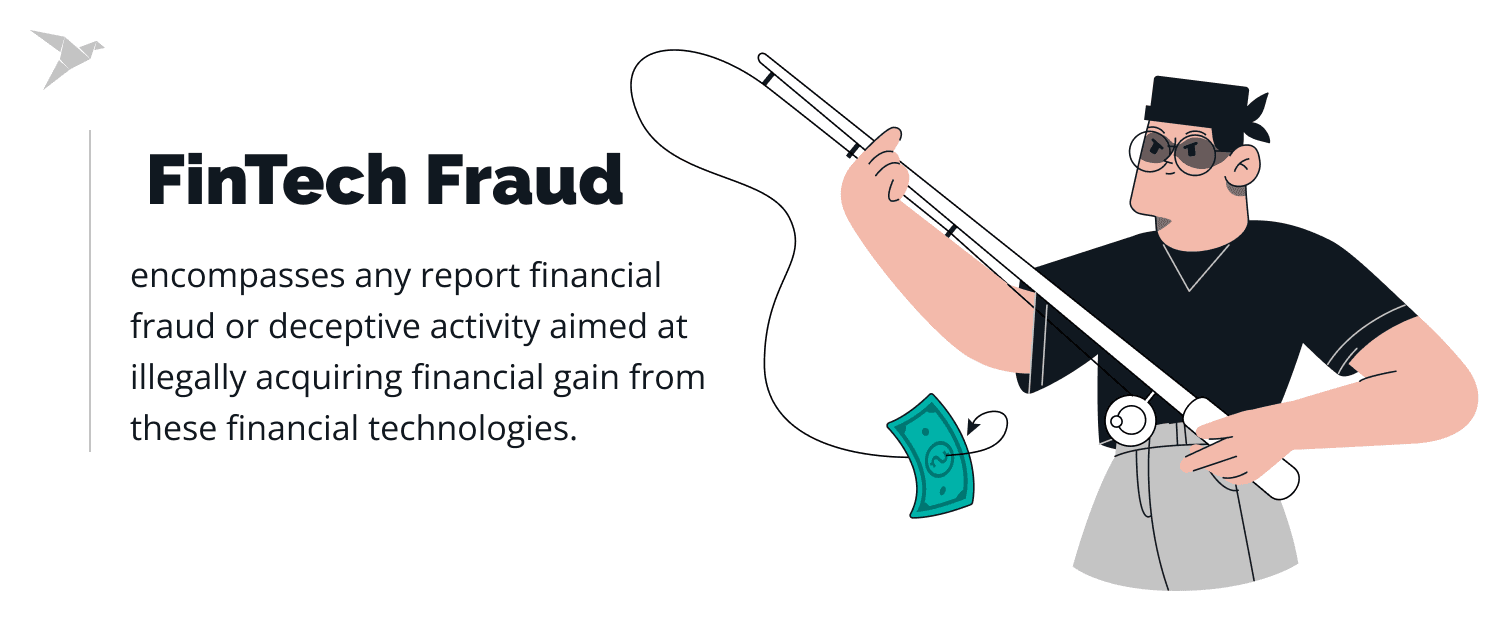

Simply put, FinTech fraud encompasses any report financial fraud or deceptive activity aimed at illegally acquiring financial gain from these financial technologies. This includes types of financial fraud like:

- Stealing login credentials to access and drain bank accounts.

- Making unauthorized charges or transferring funds without your knowledge.

- Creating fake investment opportunities to trick individuals into investing.

- Using stolen personal information to open fraudulent accounts.

- Exploiting vulnerabilities in FinTech systems to manipulate data or steal funds.

But how does FinTech fraud differ from traditional financial fraud?

While traditional methods like check forging and credit card skimming still exist, FinTech introduces unique vulnerabilities:

- Digital Identity: Our reliance on online accounts and digital identities makes them prime targets for hackers.

- Speed and Automation: Fast transactions and automated processes can mask fraudulent activity, making detection harder.

- Emerging Technologies: New FinTech solutions often have security gaps as they mature, leaving them susceptible to exploitation.

- Data Concentration: Large stores of financial data on centralized platforms attract attackers aiming for high-value targets.

The rise of FinTech fraud highlights the need for vigilance and proactive measures to protect ourselves and our finances. In the next section, we'll explore common types of FinTech fraud and how you can safeguard yourself and your assets.

While you're here - would you like to get a digital banking trends report?

What Might Be Consequences of Financial Fraud: Beyond Stolen Money

Financial fraud isn't just about losing a few bucks; it's a web of deceit with far-reaching consequences that impact individuals, businesses, and even entire economies. Here's a breakdown of the potential fallout:

Individual Victims

- Financial Loss: The most immediate impact is the direct financial loss, which can range from manageable inconveniences to life-altering situations. According to the FBI's Internet Crime Complaint Center (IC3), in 2022 alone, reported financial losses due to fraud exceeded $8 billion in the US, highlighting the sheer volume of stolen funds.

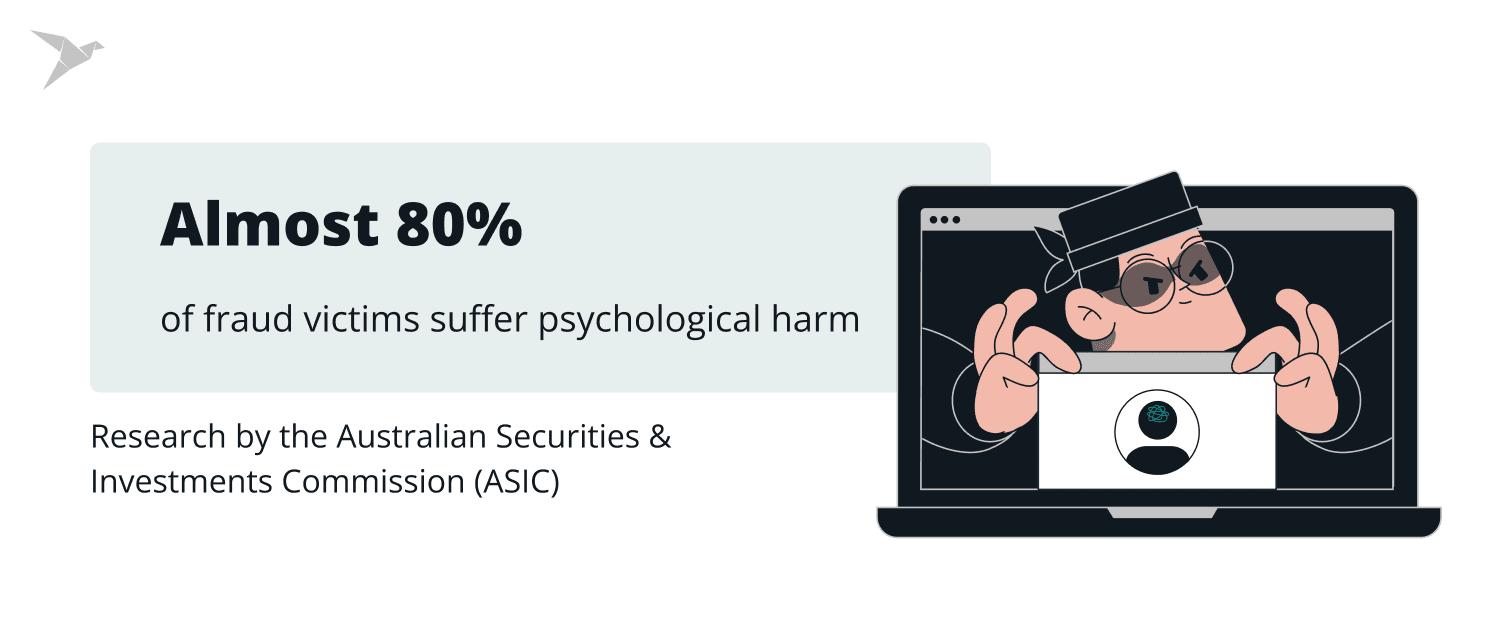

- Emotional Distress: Fraud victims often experience stress, anxiety, and even depression due to the violation of trust and the uncertainty surrounding financial recovery. Research by the Australian Securities & Investments Commission (ASIC) shows that almost 80% of fraud victims suffer psychological harm, with many experiencing sleep disturbances, appetite changes, and difficulty concentrating.

- Identity Theft: Stolen information can be used to open new accounts, take out loans, or make purchases, leading to further financial burdens and credit rating damage. A 2023 study by Javelin Strategy & Research found that identity theft victims spend an average of 200 hours resolving the issue, demonstrating the significant time commitment required for recovery.

Business Repercussions

Financial Penalties: Businesses caught engaging in fraudulent activities face hefty fines and legal fees, potentially jeopardizing their financial stability. In 2022, the Financial Conduct Authority (FCA) in the UK issued over £2.2 billion in fines for financial misconduct, showcasing the consequences of negligence investment fraud or malpractices.

Reputational Damage: News of fraud can severely damage a company's reputation, eroding customer trust and loyalty. A study by PwC found that 73% of consumers lose trust in a brand after experiencing fraud, demonstrating the long-term reputational damage businesses can face.

Operational Disruptions: Investigating and mitigating fraud can divert resources away from core business operations, impacting productivity and efficiency. According to the Association of Certified Fraud Examiners (ACFE), businesses lose an average of 5% of their annual revenue to fraud, highlighting the significant economic impact on organizations.

Learn about our expertise in the industry and what we have to offer

Societal Impact

- Erosion of Trust: Widespread financial fraud can erode public trust in financial institutions and markets, hindering economic growth and stability. A 2021 survey by Edelman found that only 54% of people globally trust financial institutions, underscoring the need for robust measures to rebuild trust.

- Loss of Government Revenue: Fraudulent activities like tax evasion or money laundering deprive governments of vital revenue needed for public services and infrastructure. The European Commission estimates that tax evasion costs EU member states €1 trillion annually, showcasing the significant fiscal impact on governments.

- Funding of Criminal Activities: Proceeds from financial fraud can be used to fund organized crime, terrorism, and other illegal activities, posing a threat to public safety and stability. A 2020 report by the United Nations Office on Drugs and Crime (UNODC) estimated that the global illicit economy generates between $2.3 trillion and $3.6 trillion annually, highlighting the link between financial crime and broader societal issues.

Remember: These are just a few examples, and the specific consequences of financial fraud can vary depending on the type of fraud, the individuals involved, and the wider context of committing fraud. However, it's crucial to recognize the seriousness of this issue and take proactive steps to protect ourselves and our communities.

Who Is Vulnerable To FinTech Fraud?

Unfortunately, no one is truly immune to FinTech fraud. While some demographics might be statistically more targeted, the nature of FinTech makes it a potential threat to anyone who interacts with these technologies.

Beyond Stolen Money: Broader Vulnerabilities for Businesses:

- New Entrants: FinTech startups often prioritize speed to market over robust security, leaving them susceptible to data breaches and exploitation.

- Complex Ecosystems: Integrated platforms and partnerships create interconnected vulnerabilities, increasing the potential attack surface.

- Emerging Technologies: Rapidly evolving technologies like cryptocurrency and artificial intelligence introduce novel attack vectors that require vigilance.

- Compliance Burdens: Keeping up with regulatory requirements and data privacy laws adds complexity, potentially diverting resources from robust security strategies.

- Insider Threats: Disgruntled employees or compromised accounts present internal risks that require robust access controls and monitoring.

While any business can be targeted, some are inherently more susceptible:

- Small & Medium-Sized Enterprises (SMEs): Limited resources and security expertise leave them vulnerable to basic attacks.

- Businesses in High-Risk Industries: Money transfer, online gambling, and cryptocurrency exchanges attract sophisticated fraudsters.

- Data-Rich Companies: Businesses handling sensitive financial data are prime targets for identity theft and data breaches.

- Globally Operating Businesses: Navigating diverse regulations and cultural norms adds complexity to security strategies.

Remember: Vigilance is key. Don't wait for an attack to happen – act now to protect your data, your reputation, and your bottom line.

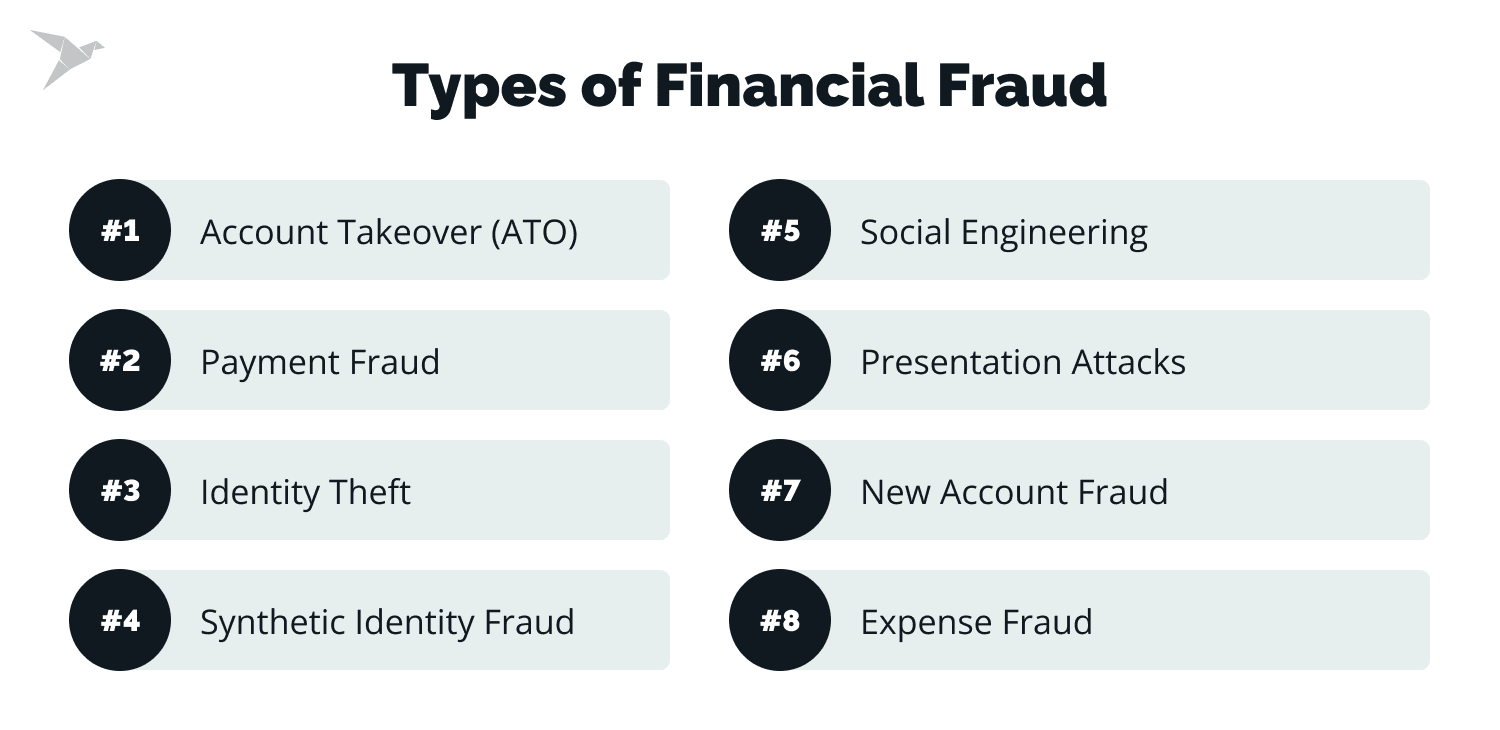

Types of Financial Fraud

Here's a concise overview of some of the most prevalent FinTech fraud schemes:

Account Takeover (ATO)

Account Takeover involves fraudsters gaining control of an online account using stolen credentials. This can lead to various fraudulent activities, such as unauthorized fund transfers, payments, or the opening of new accounts in the victim's name. ATOs not only result in financial losses for consumers but also pose challenges for banks, impacting their reputation and customer loyalty.

In 2022, ATO fraud resulted in staggering losses amounting to $11 billion. Hackers employ various methods like phishing emails, malware, or credential stuffing to steal login credentials. Once in, they can drain funds, transfer assets, or even hijack multiple accounts together for further criminal activity.

To execute ATO fraud, bad actors exploit information from data breaches and employ credential-stuffing software to breach financial accounts. For instance, data obtained from a streaming service or data breach might yield login details that fraudsters test across various accounts using bots, enabling them to test numerous account-password combinations within seconds. Once access is gained, fraudsters can manipulate account information, effectively locking out legitimate owners.

Real-world Example: In 2022, a major social media platform experienced a large-scale ATO attack, compromising millions of user accounts. Hackers used a combination of phishing emails and credential stuffing to gain access, resulting in significant financial losses and reputational damage.

Payment Fraud

This encompasses a spectrum of deceptive activities aimed at stealing or manipulating payments. Fake transactions can appear on your statement, unauthorized charges on credit card statements might be disguised as legitimate fees or taxes, and stolen payment information can be used for online purchases.

Fraud scenarios are diverse, ranging from fraudulent online marketplace transactions demanding payment through P2P apps without delivering the promised goods to using stolen credit card number and information for personal purchases via P2P accounts. Since 2016, incidents of P2P payment fraud victims have skyrocketed by an alarming 733%, presenting a significant challenge given the absence of comprehensive policies within most P2P apps to shield users from fraud losses due to scams. Moreover, P2P fraud serves as a gateway to more severe threats like account takeovers.

Identity Theft

Identity theft encompasses fraud committed by stealing personal information, including name, birthday, and Social Security number (SSN). Identity thieves exploit this information to gain unauthorized access to accounts, resulting in drained bank accounts, fraudulent loans, or maxed-out credit cards. This involves stealing personal information like Social Security numbers or credit card details to open new accounts, obtain loans, or make purchases in your name.

Identity theft occurs when fraudsters exploit personal information to gain unauthorized access to accounts. They may acquire your credentials through dark web purchases, data breaches, or phishing attacks. Examples of bank fraud resulting from identity theft include unauthorized password changes, fraudulent payments, bank statements, or money transfers to other accounts. If your credit card details are compromised, you may observe suspicious charges on your account.

Synthetic Identity Fraud

Synthetic identity fraud occurs when fraudsters blend authentic personal data, such as a valid social security number, with fabricated or false information elsewhere, like a new name or date of birth. This amalgamation creates a synthetic identity used to circumvent identity verification checks when registering for financial accounts. The primary targets of this types of financial fraud are often children, the elderly, and unhoused individuals, who may be less vigilant in credit usage and monitoring. For instance, a fraudster might pilfer a genuine social security number and then invent associated details like a name, date of birth, address, email, and phone number.

This sophisticated scheme creates entirely fictitious identities using fabricated information. Fraudsters then use these identities to open accounts, obtain credit cards, and commit other financial crimes.

Social engineering

Social engineering involves manipulating victims into disclosing sensitive information, such as account passwords or transferring funds, often through irreversible means like real-time payments or cryptocurrency transactions.

For instance, hackers might impersonate a legitimate entity, like a payroll company, through deceptive emails, prompting recipients to disclose their bank account number or details on fraudulent websites. Combatting social engineering begins with educating employees and customers about phishing schemes and leveraging encryption and multi-factor authentication tools like Plaid to secure data.

Presentation Attacks

Presentation attacks occur when fraudsters exploit someone else's physical traits or biometric data, such as fake fingerprints or photos, to impersonate them and gain access to online accounts. For example, if a banking app utilizes facial recognition, fraudsters may use high-quality photos or deep fake technology to create a convincing likeness of the victim's face.

By presenting the fake version during login, they circumvent facial recognition and access the victim's account for fraudulent purposes. Preventing presentation attacks requires robust defenses against common tactics, including data validation, government ID checks, and advanced liveness checks.

New Account Fraud

New Account Fraud, also referred to as advance fee fraud, account creation fraud, wire transfer,, account opening fraud, or fake account fraud scam, is a prevalent form of bank fraud. It involves a fraudster or money mule opening an account with the intention of committing fraudulent activities, often using stolen or synthetic identities.

Fraudsters acquire identities through data breaches, phishing, or may even exploit information belonging to vulnerable individuals such as children, the deceased, or the homeless. In some instances where police report a financial fraud, individuals known as mules may employ their own identities for fraudulent purposes, constituting first-party fraud.

Expense Fraud

Expense fraud involves deliberately submitting inaccurate or inflated expense reports with the aim of receiving reimbursement from an employer for personal expenses. This deceit may encompass claiming reimbursement for expenses that were never incurred, and employees might also exaggerate the costs of legitimate expenses to secure a larger reimbursement.

While traditional expense fraud involved inflated mileage claims or pilfering petty cash more customers, today's landscape investment fraud presents a broader spectrum of threats:

- Fictitious Expenses: Fraudsters create entirely fabricated expense reports claiming travel, meals, or other costs that never occurred.

- Inflated Costs: Receipts are manipulated to overcharge for legitimate expenses, pocketing the difference.

- Duplicate or Split Invoices: Legitimate invoices are submitted twice or split into smaller amounts to evade approval thresholds.

- Ghost Employees: Fake employee identities are created to submit fraudulent expense reports.

- Collusion Schemes: Employees collaborate with vendors or external parties to submit false claims.

Wrapping up

By implementing the key steps outlined in this comprehensive guide, you can build impregnable defenses against FinTech fraud. Remember, this journey requires continuous effort and adaptation. Stay informed about emerging threats, embrace new technologies, and foster a culture of security awareness within your organization.

However, your efforts alone are not enough. Collaboration with industry peers, security experts, and regulatory bodies is crucial for sharing insights, best practices, and intelligence to stay ahead of the curve. By uniting forces, we can create a more secure and resilient FinTech ecosystem for everyone.

Remember: As technology advances, so too must our defenses. Embrace innovation, invest in your security posture, and empower your people to be active participants in safeguarding your FinTech future. Together, we can build a digital landscape where innovation thrives alongside trust and security.

Beyond this guide: explore additional resources, industry publications, and security blogs to stay updated on the latest threats and best practices. Remember, the fight against FinTech fraud is a continuous journey, and continuous learning is key to success.

FAQ

FinTech fraud prevention is crucial to safeguarding financial transactions in the digital era. It ensures the integrity of the FinTech ecosystem, protecting users, businesses, and the financial industry from malicious activities, maintaining trust, and fostering a secure financial environment.

Several common fraud schemes pose threats. These include account takeover (stealing logins to drain funds), payment fraud (unauthorized charges or fake transactions), investment fraud (Ponzi schemes, pump-and-dumps), identity theft (using stolen data for new accounts), and synthetic identity fraud (creating fictitious identities for fraudulent activity).

User education is vital to empower individuals with the knowledge and skills needed to recognize and thwart fraud attempts. Training on identifying phishing attempts, promoting safe online practices, and enhancing cybersecurity awareness contributes to a resilient line of defense against evolving fraud tactics.

The future of FinTech fraud prevention is poised for advancements in artificial intelligence, machine learning, and collaborative information sharing. Predictive analytics, biometric authentication, and real-time monitoring services will play pivotal roles, offering proactive defense mechanisms against emerging fraud threats in the evolving digital landscape.